- The first step is making the call.

- 1300 022 482

- hello@searchpartyproperty.com.au

As of 31st July 2022 – Property Market Update

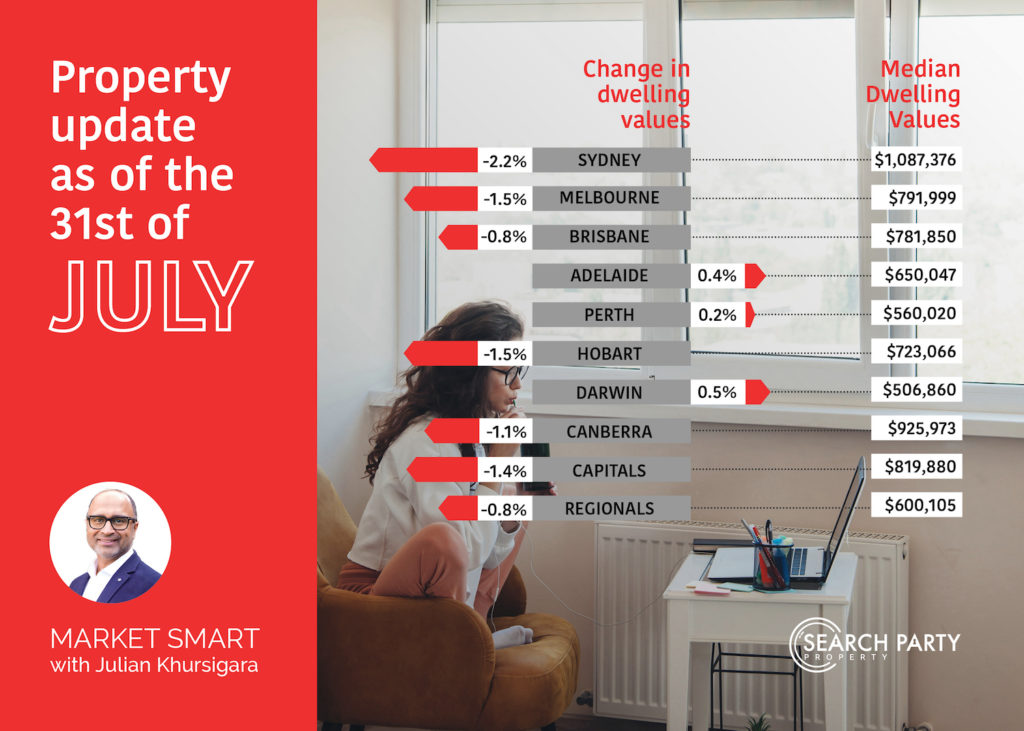

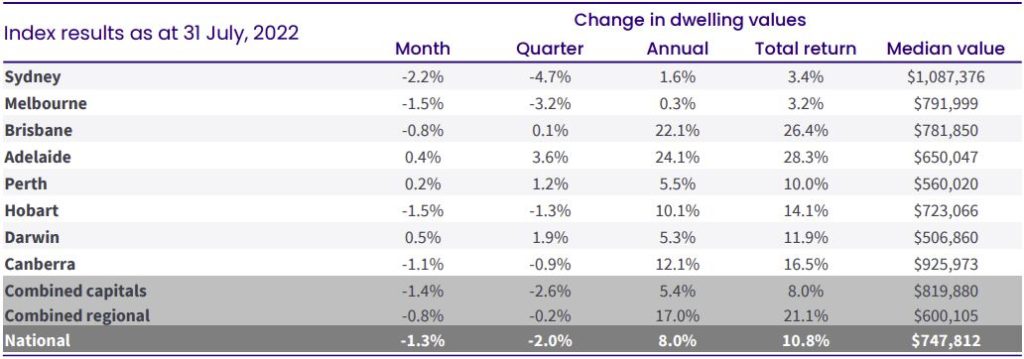

The national median dwelling value has fallen for the third consecutive month, with property prices down 1.3% over July. Worryingly, this downswing seems to be gaining speed with more markets moving into negative territory and larger drops being recorded.

Once again, Sydney is leading the trend, with median prices down 2.2% over the month, and 4.7% over the quarter. This is the sharpest downturn in property prices the harbour city has seen in almost four decades.

Melbourne is not far behind, with median prices down 1.5% over July, and 3.2% over the quarter. The median property price also declined in Hobart and Canberra, which were down 1.5% and 1.1% (respectively) over the month. The Brisbane market has also slowed significantly, slipping into negative territory for the first time since August 2020.

But it is not all bad news, with a few capital city markets continuing to record modest growth. Specifically, Perth (up 0.2%), Adelaide (up 0.4%), and Darwin (up 0.5%) have managed to remain in positive territory. That said, the rate of growth in all three of these markets has slowed significantly since the start of the year.

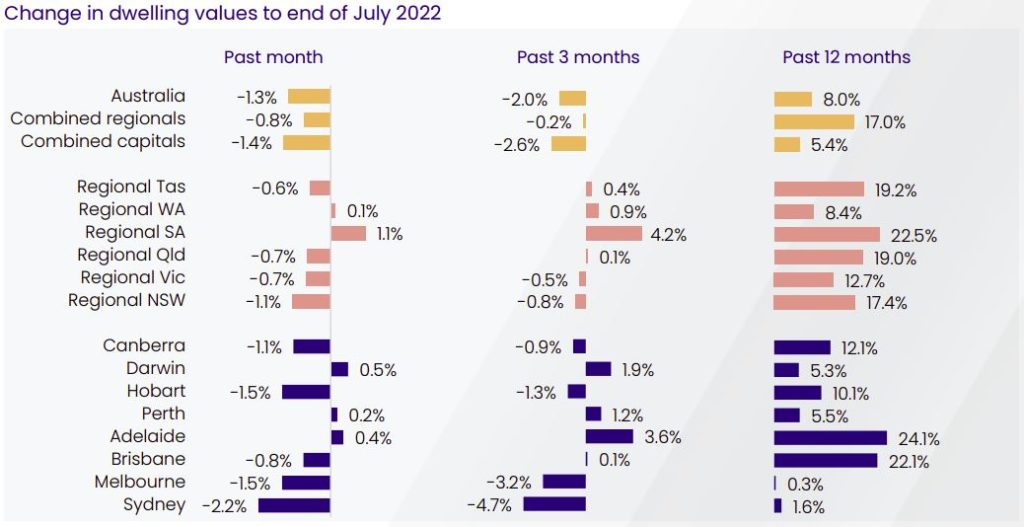

Outside the capitals, the story is fairly similar, with the combined regional median dwelling value down 0.8% over the month. This is the first time this measure has declined since August 2022.

This decrease is largely being driven by notable drops in Regional NSW (down 1.1%) and Regional Victoria (down 0.7%). That said, Regional Queensland (down 0.7%) and Regional Tasmania (down 0.6%) also saw negative growth numbers for the month. Only Regional WA (up 0.1%) and Regional SA (up 1.1%) managed to buck the trend and remain in positive growth territory.

Importantly, most of the “lifestyle locations” that received significant interest over the last few years have also recorded declining values. Areas like the Southern Highlands, Ballarat, and Gold and Sunshine Coast have all seen negative monthly and quarterly growth numbers. Given the significant gains these regions experienced recently, this is a clear sign of how much the market has slowed.

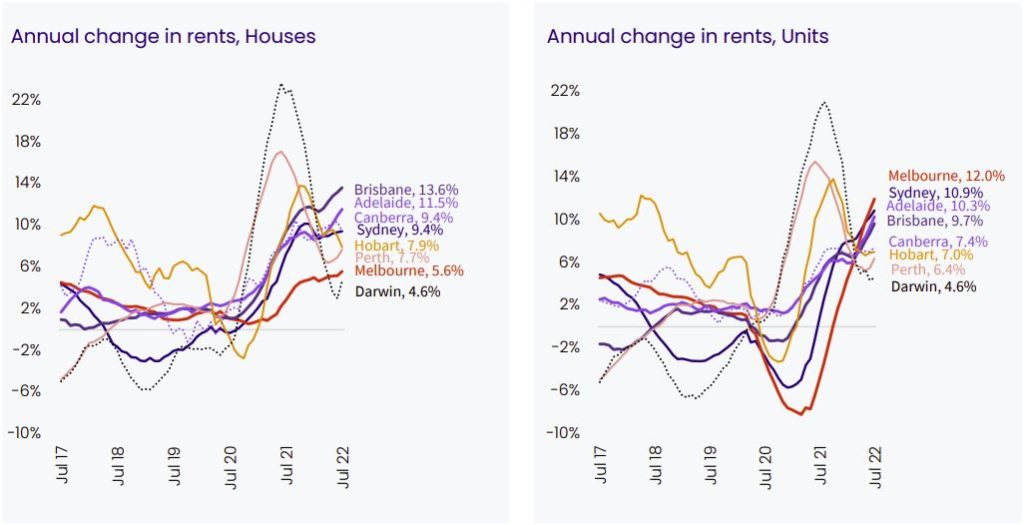

On the rental side, most markets remain extremely tight, and this is continuing to put upward pressure on rent rates. The national median rent rose 0.9% over July, putting it 2.8% up over the quarter and 9.8% up over the year. This is largely being driven by ongoing supply issues, with available rental volumes down roughly one-third on the 5-year average.

What lies ahead

In particular, many experts are expectantly watching movements in:

- Interest rates: The Reserve Bank of Australia (RBA) has again decided to raise the cash rate by 0.5%, bringing it to 1.85%. This was largely in line with predictions and at least partly driven by recently released inflation figures. However, all signs suggest this will not be the last increase, and thoughts on how high rates will rise vary.

- Supply of new listings: Typically, as the weather warms up, so does the property market, with more properties advertised for sale. While current listing volumes vary greatly depending on the location, they have generally been following the standard seasonal trends. However, with such uncertainty in the market, homeowners could be hesitant to sell, potentially reducing available stock and increasing competition.

- Affordability: Many experts believe that affordability issues were a major factor in the slowing of recent price growth. But, with prices now declining in most areas, affordability should – at least theoretically – be increasing. However, with the cost of living increasing and lending conditions tightening, affordability may continue to be a problem for buyers.

- Investor interest: As astute property investors know, the best time to find a great deal is generally when the market is falling. We are seeing this at the moment, with investor activity increasing across several key market segments. However, lending conditions and affordability concerns may soon start impacting investors too, which could further slow sales rates.

Suburb Spotlight: Shepparton (VIC)

Over the last century or so, Shepparton has earned a reputation as a highly industrious regional centre. This is largely thanks to the area’s longstanding connection to manufacturing and transportation, sectors that continue to be major local employers. However, there is a lot more to Victoria’s 6th largest city than just the local processing and production facilities.

Shepparton sits at the heart of the Goulburn Valley, about 185km north-northeast of the centre of Melbourne. As the civic and commercial centre of the Greater Shepparton region, it is well served by a range of amenities. There is a flourishing food and wine scene; multiple primary, secondary, and tertiary education campuses; and a thriving arts community.

Despite all this, Shepparton remains relatively affordable, with the median house price currently sitting just below $400,000. This reflects the fairly modest rate of capital growth properties in the area have seen over the last couple of decades. But, with the population of Greater Shepparton expected to increase by 25% over the next 15 years, this could soon change.

One of the biggest appeals of Shepparton, at least for investors, is the potential rental returns on offer. While these vary depending on a property’s exact location, yields of 5% or more are possible in many areas.

That said, investors looking for more balanced returns are best to focus on the newer estates to the city’s north. Over the last couple of years, suburbs like Kialla have seen some of the region’s best capital growth numbers. And while rental yields are slightly lower than some neighbouring areas, they still generally exceed 4%.

At Search Party Property, we specialise in developing tailored investment strategies and will work with you to come up with a suitable plan of attack. We also regularly assess your strategy ensuring that it is fit for purpose and delivering the desired results.

{kind=link}

{kind=link}