Market Trends

August Market Smart:

Growth Holds, But the Heat Is Fading

Mid-sized capitals shine as Sydney and Melbourne cool. Is this the start of a new market phase?

Australia’s housing market notched another month of growth in August, but the pace is slowing. Perth, Adelaide, and Darwin continue to lead the way, while affordability pressures weigh on Sydney and Melbourne.

Rental growth is softening in major cities, and buyer urgency is easing — but there are still clear opportunities for investors.

Key Take Aways

National home values post strongest rise in a year

Home values rose 0.7% nationally, the strongest monthly increase in over a year, with annual growth now at 4.1%.

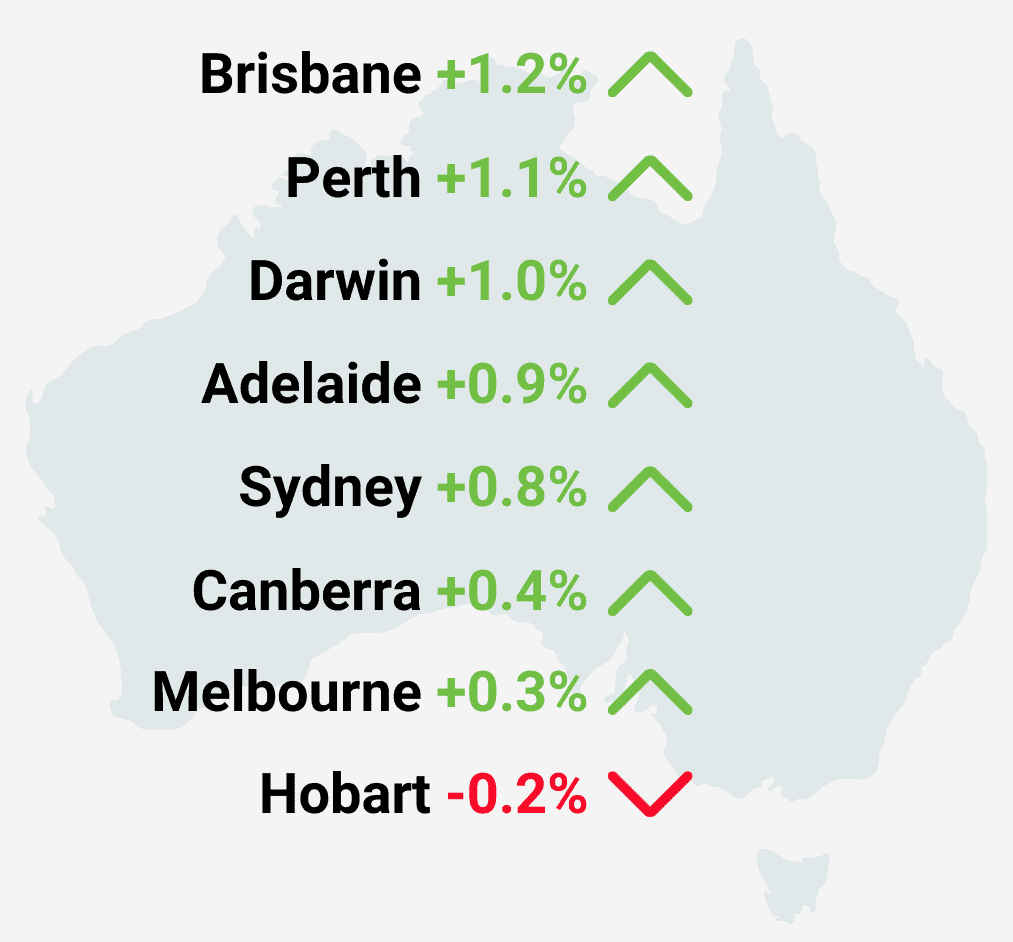

Brisbane leads market gains

Mid-sized capitals remain the top performers, led by Brisbane (+1.2%), Perth (+1.1%), Adelaide (+0.9%), and Darwin (+1.0%).

Spring listings up, supply still tight

Listings are rising into spring, but advertised stock remains ~20% below average, keeping market conditions competitive.

Auction clearances at 70%

Auction clearance rates hit 70%, the highest since early 2024, a clear sign of buyer confidence.

Rents climb as vacancies tighten

Rents rose 0.5% in August, with tight vacancy rates (1.5%) driving continued pressure on rental markets.

Darwin leads in rental yields

Darwin leads rental growth and yields, with a 6.5% gross rental yield and strong investor interest.

Consumer sentiment hits 3.5 year high

Consumer sentiment reached a 3.5-year high, supported by easing interest rates and cost-of-living pressures.

Wages rise 1.3%

Real wages are growing at a rate of 1.3% annually, helping to boost purchasing power and household confidence.

Home guarantee scheme launches in October

The new Home Guarantee Scheme launches in October, reducing deposit requirements and removing caps for FHBs.

Growth moderates amid caution

Affordability and cautious lending will continue to moderate growth, but momentum is expected to carry through the spring.

Market Trends

If February marked the turning point, then August may be the moment momentum took hold. National housing values continue their climb, with the pace of growth accelerating into spring. Demand is rising, confidence is strengthening, and borrowing capacity is improving — but supply remains the missing piece. The imbalance between demand and supply is once again the dominant force shaping housing market outcomes.

Let’s unpack the month that was.

Where are we now?

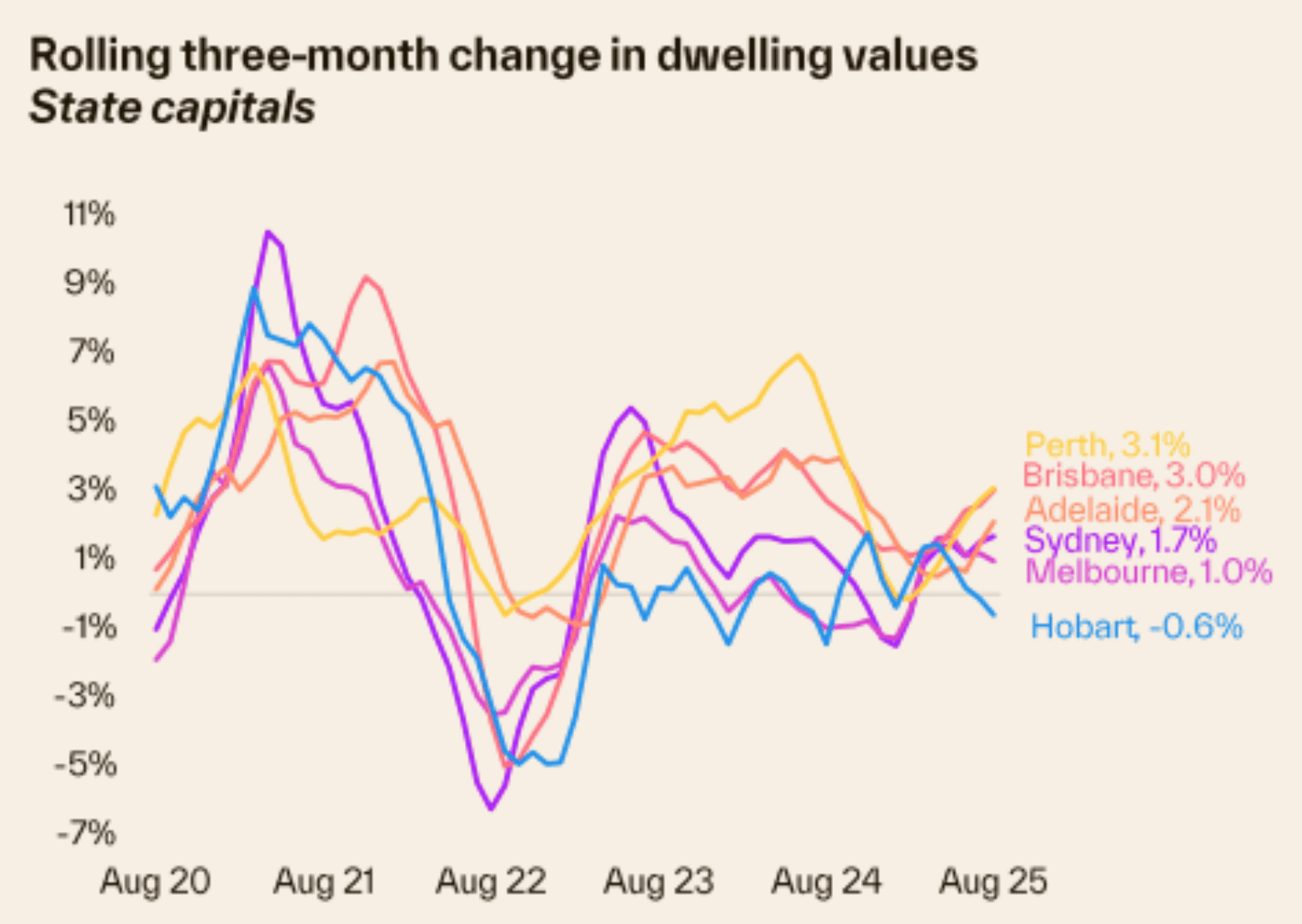

Australia’s housing market extended its growth streak in August, with Cotality’s national Home Value Index rising 0.7%, the strongest monthly increase since May last year. This marks the second month in a row of rising annual growth, which now sits at 4.1%.

Importantly, the upswing continues to broaden geographically:

- Brisbane (+1.2%), Perth (+1.1%), and Adelaide (+0.9%) once again led the capitals.

- Darwin posted an impressive +1.0%, taking year-to-date gains to 10.8% — the strongest of any city.

- Hobart was the only capital in decline, down 0.2%.

Cotality, 2025

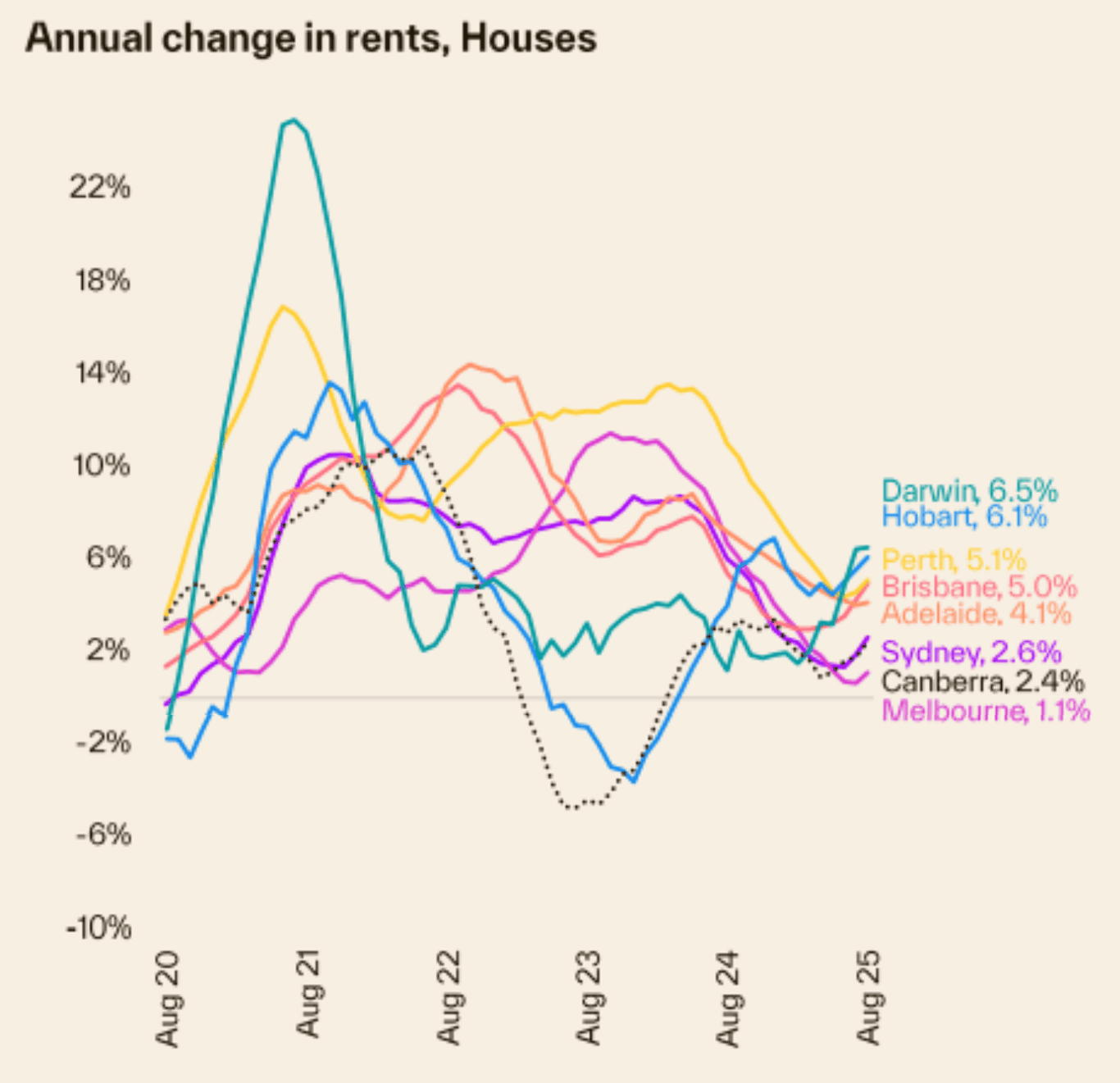

On the rental front, national rents lifted 0.5% in August, the fastest rise since May 2024. Annual rental growth also rose to 4.1%, suggesting a fresh upswing may be underway. Darwin is again the standout performer, with gross rental yields now sitting at 6.5%. At the other end of the scale, Sydney and Melbourne recorded the weakest rental growth, but the trend appears to be picking up.

Other key signals:

- Vacancy rates remain at 1.5%, well below historical norms.

- Auction clearance rates hit 70% in late August, the highest since early 2024.

- New listings are rising, as expected in spring, but advertised stock remains ~20% below average — keeping competition among buyers strong and vendor conditions favourable.

Cotality, 2025

How did we get here?

This growth cycle has been quietly building since the RBA’s rate cut in February, and August shows clear signs of gathering momentum.

- Real wages are growing again, up 1.3% annually — the strongest result since 2020.

- Consumer sentiment hit a 3.5-year high in August, buoyed by easing cost-of-living pressures and the improving interest rate outlook.

- Households are saving again, as the savings ratio trends back to pre-pandemic norms, giving buyers more firepower.

- Employment remains tight, with the jobless rate below 4% and underemployment at 5.9%, well below average.

- Mortgage stress and defaults remain low, helped by stable employment and a lack of negative equity.

This supportive economic backdrop has aligned with tight supply, and that’s been key. Estimated home sales are now 2% higher than a year ago and 4% above the five-year average, yet stock on market remains stubbornly low. As Tim Lawless of Cotality notes, “we are seeing a clear mismatch between available supply and demonstrated demand.”

Where are we going?

What’s driving the outlook?

Tailwinds:

- A stronger household sector: better wages, sentiment, and savings.

- A tight labour market, supporting serviceability.

- Low vacancy rates and high rents supporting investor interest.

- Ongoing momentum in key mid-sized capitals.

New stimulus is also about to arrive:

As we move deeper into spring, the key dynamic remains unchanged: strong demand meets limited supply. That’s a recipe for continued growth, albeit likely at a sustainable, rather than spectacular, pace.

The expanded Home Guarantee Scheme, starting October 1st, removes income caps and offers unlimited places, making it easier for FHBs to enter the market with just a 5% deposit, especially significant in expensive markets like Sydney.“Saving a 5% rather than a 20% deposit could shave around

10 years off the time it takes to buy,” says Lawless.

Headwinds:

- Affordability remains stretched — particularly in Sydney and Melbourne.

- Interest rates, while falling, are still 350 basis points above pandemic lows.

- Elevated household debt and cautious lending practices will keep a lid on runaway growth.

- Population growth is now stabilising, taking some pressure off demand in the medium term.