Market Trends

July 2025 Market Smart:

Why the Market Still Has Room to Run: July’s Property Market Snapshot

National prices rise for the sixth month in a row, with low supply and stronger sentiment keeping the recovery on track.

Despite affordability constraints, the market continues to edge higher supported by tight listings, rate cuts earlier this year, and growing buyer confidence. This month’s Market Smart breaks down the performance by city, the key structural forces at play, and what smart investors should be watching.

Key Take Aways

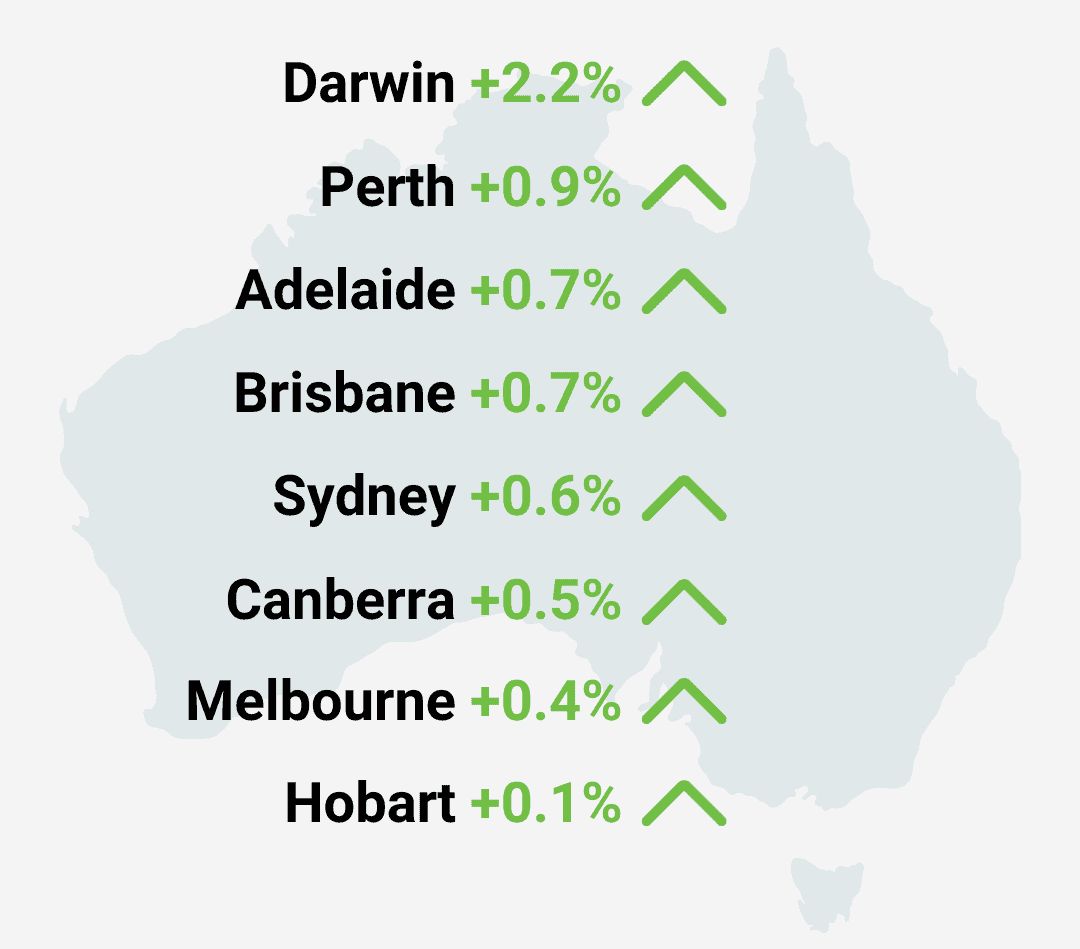

National home values rose in every capital

National home values rose 0.6% in July, in line with June’s growth, showing consistent upward momentum.

Every capital city posted positive growth

Led by Darwin (+2.2%) and Perth (+0.9%).

Strongest rate increase since 2024

The national quarterly growth rate lifted to 1.8%, the strongest since June 2024.

Houses outperform units

House values are rising faster than units, with a growing price gap of 32.3% nationally.

Listings remain low

Listings remain 19% below the 5-year average, keeping upward pressure on prices.

Strong sales activity

Annual sales activity is 1.9% above average, signalling solid underlying demand.

Strong buyer confidence

Auction clearance rates are tracking above the decade average, pointing to improving buyer confidence.

Market Trends

Australia’s property market has entered a more balanced phase, but growth remains resilient. The 0.6% rise in national values for July mirrors gains seen in May and June, suggesting the market has found a stable rhythm. This marks the sixth consecutive month of growth — momentum that began with the RBA’s rate cut in February. While the pace of gains isn’t accelerating, it’s proving to be remarkably consistent, despite affordability constraints.

The quarterly growth rate of 1.8% is the strongest in over a year, pointing to a clear upswing. Demand remains steady, supported by improving sentiment and falling rates. But it’s the chronic undersupply, with listings still 19% below average — that’s doing the heavy lifting. In short, there may be limits on how fast the market can grow, but not on whether it continues to grow at all.

Darwin and Perth Take the Lead, But All Capitals Are Moving Up

July saw broad-based growth across the capital cities, but the standout was Darwin, posting a 2.2% monthly gain — its strongest result this year and part of a 9.7% year-to-date upswing. While Darwin’s small market size limits its influence on national trends, its performance reflects a clear upswing.

Perth’s 0.9% rise is more significant nationally. It marks the city’s fastest rate of growth since September 2024, confirming it as one of the most consistently performing markets this cycle. Even softer performers like Hobart (+0.1%) and Melbourne (+0.4%) remained in positive territory, underscoring the market’s breadth of strength this month.

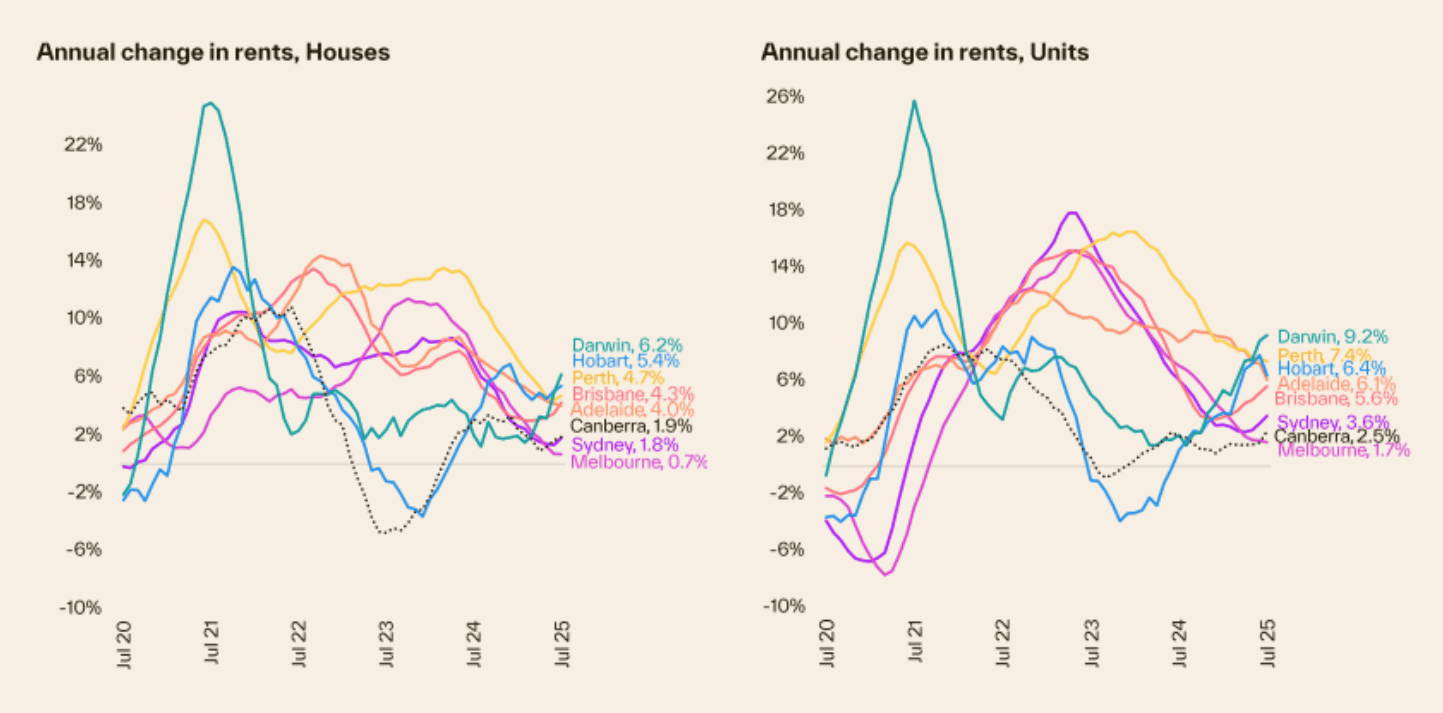

Annual change in rents

Cotality, 2025

Low Listings Keep Pressure on Prices

Cotality reports that national listings are 19% below the five-year average, helping to support values even in the face of high prices and tighter borrowing capacity. The supply-demand imbalance is most pronounced in cities like Perth and Adelaide, where listings are particularly scarce. This tight inventory environment has also helped boost auction clearance rates, which have tracked above the decade average since mid-May. With buyers competing over a limited pool of properties, vendors are holding firm on price, and time on market remains low.

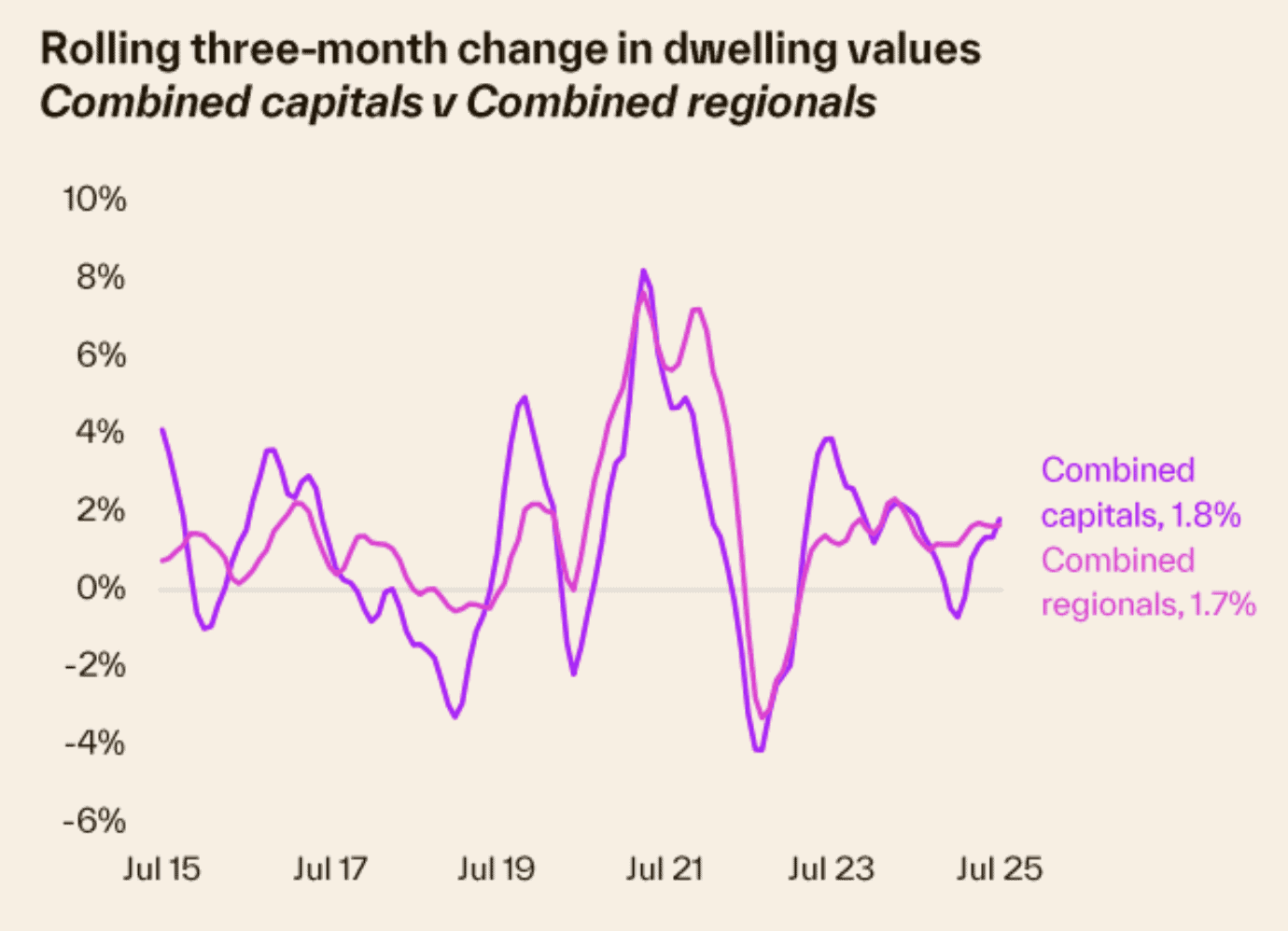

Quarterly Growth Rebounds, With Capital Cities Back on Top

The rolling quarterly gain hit 1.8% nationally, its strongest since mid-2024. For the first time in 10 months, the combined capitals (1.8%) are outperforming the combined regionals (1.7%), reversing the regional-led trend of late 2024 and early 2025. However, regional markets are still performing well, with regional QLD (+2.5%), SA (+2.0%) and VIC (+1.4%) all outpacing their capital city counterparts. This suggests strength isn’t isolated to major metros, it’s concentrated where affordability and lifestyle appeal intersect.

Dwelling Values

Cotality, 2025

Detached Housing Pulls Ahead of Units

Detached homes are again leading the charge, with house values up 1.9% over the quarter, compared to 1.4% for units. The median house has gained about $16,700, while the median unit rose just $9,700. This divergence reflects both buyer preference and borrowing power, as interest rates fall, higher-income households can unlock greater capacity, often preferring standalone homes. As a result, the price gap between houses and units has stretched to a record 32.3%, or about $223,000. Despite affordability pressures, demand for detached housing remains dominant.

Demand Holds Firm Despite Macro Headwinds

Cotality’s estimates show annual sales volumes are now 1.9% above the five-year average, indicating healthy, if not booming, demand. This is a strong result considering the current interest rate environment. Combined with low listings, this sales performance has kept market conditions balanced in favour of sellers, particularly in mid-tier capitals. The consistency of these numbers, across values, sales, and rental conditions, points to a market that’s moving steadily, even if not spectacularly.

What Should Investors Do?

- Invest where supply is tight: Cities like Perth and Darwin are gaining pace on the back of low listings and rebounding confidence.

- Stick to the middle rings: Suburban areas offer the best value-to-demand ratio, especially in Brisbane, Adelaide, and Melbourne.

- Back detached houses: With house values outperforming units and preferences leaning toward land, this is where capital growth is flowing.

- Act before sentiment shifts: Momentum is building, and if rate cuts accelerate later this year, competition could return sharply.