Market Trends

May 2025 Market Smart:

Values Up 1.7% in 2025

National home values continued to rise in May, albeit at a slightly softer pace than April, posting a modest increase and marking the fourth consecutive month of growth. This result compares to April’s 0.3% lift, underscoring the market’s resilience despite the recent federal election hiatus. Activity broadly normalised post-election, with listing volumes and clearance rates returning to near-seasonal averages, supporting sustained demand across both metro and regional markets.

Key Take Aways

Fourth Consecutive Month of Growth

National home values rose 0.4% in May, lifting the median dwelling value by approximately $3,050. This follows April’s 0.3% increase, suggesting that post-election confidence is feeding through into stronger market momentum.

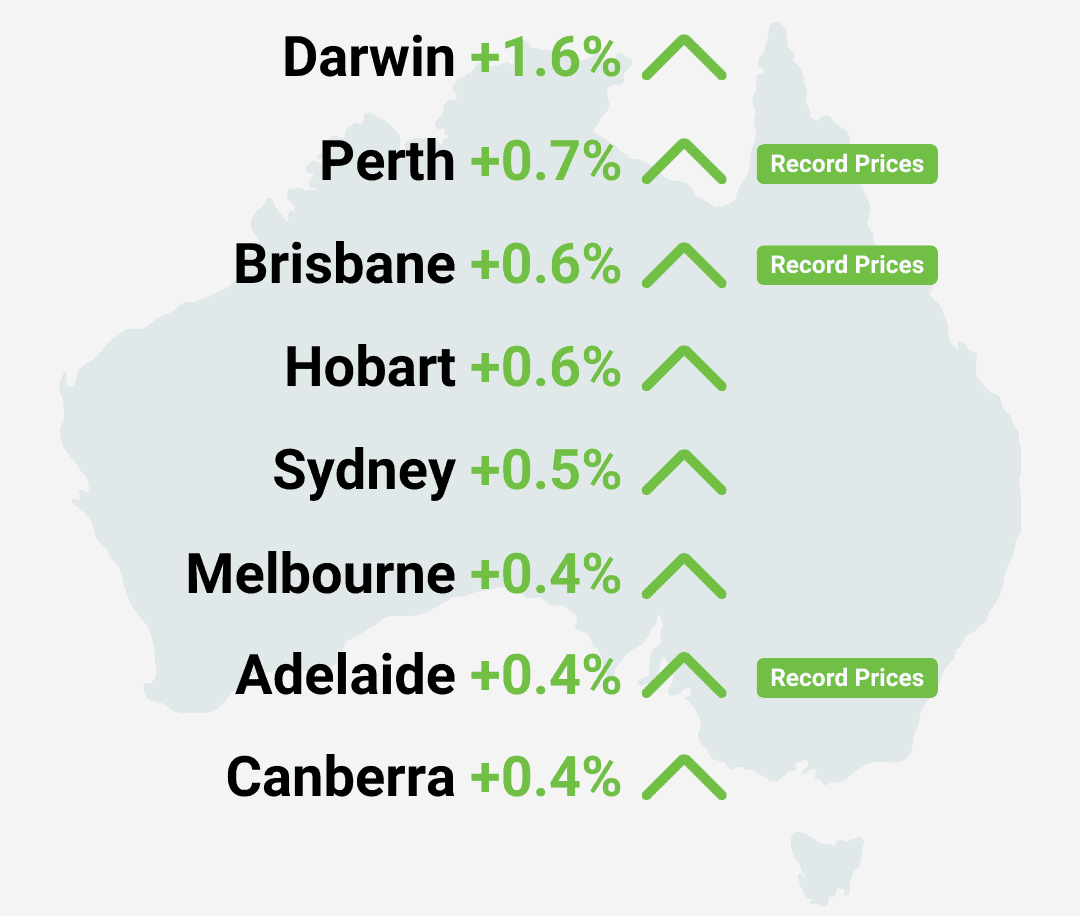

Darwin and Hobart Lead

Darwin recorded the largest monthly gain at +1.2%, while Hobart followed closely with +1.0%. Sydney and Melbourne both saw modest increases of 0.3% each. Melbourne remains roughly 5.1% below its late-2022 peak, but its recovery continues to stabilise.

Regional Markets Outperform

Combined regional areas outpaced the capitals again, rising 0.7% versus 0.3% in metropolitan markets. Regional South Australia (+1.6%) and Western Australia (+1.4%) were standouts, reflecting renewed buyer interest in affordable lifestyle regions. This “flight to lifestyle” trend persists, as many buyers seek more value outside the major cities.

Rental Yields Tick Higher

National gross rental yields rose to 3.75%, marking the strongest level in over two years. Annual rent growth eased slightly to 3.5%, down from 3.6% in April, with Sydney (1.8%) and Melbourne (1.9%) experiencing the softest annual increases. Investors in Perth and Adelaide continue to see the highest yields, buoyed by tight rental stock and solid tenant demand.

Affordability Pressures Remain

May’s data show the average household still needs about 10.4 years’ savings for a 20% deposit and would devote over 51% of gross income to repayments. Elevated living costs and slightly higher borrowing rates continue to constrain first-home buyers, even as investor activity picks up.

Change in dwelling values to end of May 2025

Cotality, 2025

Smaller Markets Lead the Charge

All capital cities recorded value gains in May, although the larger markets saw only modest lifts. Sydney and Melbourne each posted a 0.3% rise, continuing their gradual recovery. Sydney is now just 0.8% below its September 2024 peak, while Melbourne sits about 5.1% down from its 2022 high. Growth in these cities is being underpinned by improved affordability at the top end of the market and the impact of recent rate cuts, but buyer sentiment remains cautious, and serviceability pressures are still weighing on many households.

The smaller capitals again outperformed their larger counterparts. Darwin led the pack with a 1.2% increase for the month, followed by Hobart at 0.9%. Perth and Brisbane both posted solid gains – up 0.5% and 0.4% respectively – driven by affordable entry points, low stock levels and competitive rental yields that continue to draw investors and owner-occupiers. Adelaide also remained strong, lifting 0.4% in May and recording roughly 10.1% annual growth, bolstered by a tight supply environment and ongoing population growth.

Rolling three month change in dwelling values – State Capitals

Cotality, 2025

Regional Markets Outpace Capitals, Driven by Affordability and Lifestyle Appeal

Combined regional markets continued to outpace the combined capitals over the three months to May, with regionals rising 1.5% compared to a 1.0% gain across the metro areas. This sustained outperformance underscores that demand in lifestyle and affordable growth corridors remains robust, even as capital city markets gather momentum. With the federal election uncertainty now behind us and rate cuts on the horizon, buyers who had been sidelined are increasingly looking beyond the capitals in search of stronger yields and price growth.

Within the regions, South Australia and Western Australia led the charge, each recording some of the strongest three-month lifts as affordability and low stock levels drove competition. Riverside towns and smaller coastal centres saw particularly strong enquiry, fuelled by remote and hybrid work arrangements that have become firmly embedded. Meanwhile, Tasmania and parts of Queensland also enjoyed above-average gains, supported by population inflows and tight rental markets. With capital city housing still commanding a premium, many owner-occupiers and investors are seizing the opportunity to secure more value and lifestyle benefits in the regions.

Rolling three-month change in dwelling values.

Combined capitals v combined regionals.

Cotality, 2025

Rental Growth Slows, but Yields Stay Strong in Perth, Adelaide and Regional Markets

Rental market dynamics continued to shift in May. Rents rose another 0.3 percent nationally on a seasonally adjusted basis, while annual growth eased further to around 3.2 percent, down from 3.6 percent a month earlier and well below the 8.3 percent peak seen a year ago. This slowdown was most apparent in Sydney and Melbourne, where annual increases dropped to roughly 1.6 percent and 1.9 percent respectively, as the post-election lull tempered demand after the post-COVID surge.

Despite softer rent growth, gross yields remained elevated – edging down only slightly to about 3.65 percent nationally, close to a two-year high. Investors in Perth, Adelaide and many regional markets continued to enjoy the strongest returns, supported by tighter vacancy rates and relatively more affordable purchase prices.

Annual change in rents – Houses

Cotality, 2025

On the supply side, May saw a clear bounce-back in auction and listing activity now the election is behind us. Around 850 auctions were held across the capitals in the week ending May 18, up from just 644 in late April – the lowest level for that time of year since 2019. New listings climbed to roughly 22,000 properties advertised across the combined capitals in the four weeks to May 25, nudging back toward long-term seasonal norms. Even so, supply remains historically constrained, and the combination of steady buyer demand and limited stock is still placing upward pressure on prices in many markets, despite the broader momentum cooling slightly.

Things to Keep an Eye On

Auction activity in Melbourne is beginning to climb, coinciding with a price rebound:

Melbourne Auction Clearance Rate vs Price Growth

The time required to complete a property has ballooned since 2013 – particularly for houses:

Average Building Completion Times

AMP, ABS