Market Trends

June 2025 Market Smart:

Why the Smart Money Is Moving Now: June’s Property Market Wrap

Australia’s housing market continues to push higher, despite high interest rates and economic uncertainty. This month’s Market Smart breaks down where growth is happening, what’s driving it, and where investors are turning their attention next.

Rental markets remain tight, with smaller capitals experiencing rising prices, and momentum is building, albeit slowly. We unpack the data, the trends, and the opportunities for investors in the second half of 2025. Here’s what’s happening and what you should do about it.

Key Take Aways

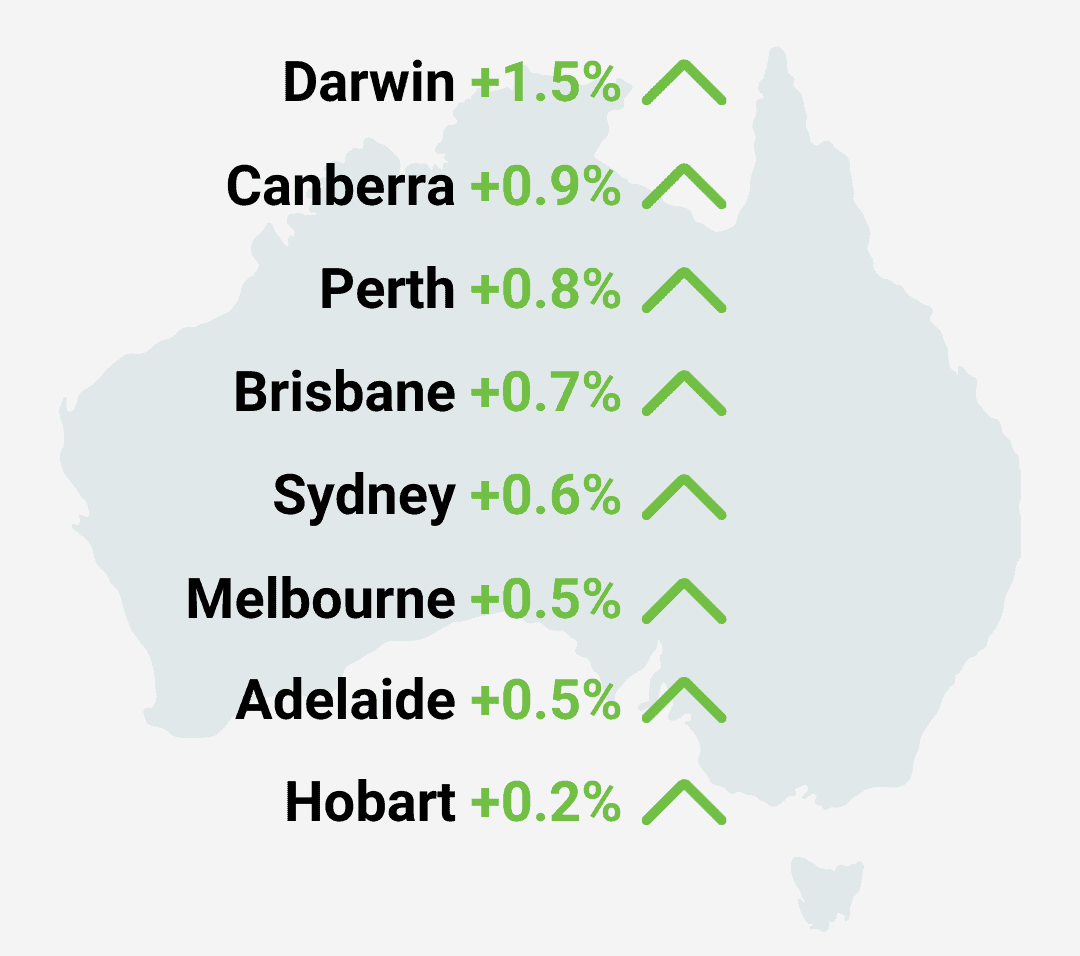

National home values rose in every capital city

National home values rose 0.7% in June, extending a ten-month growth streak.

Perth, Adelaide and Brisbane lead the Charge

Perth, Adelaide and Brisbane remain the strongest markets, driven by affordability, population growth, and supply shortages.

Rents rose 8.5%

Rents rose 8.5% over the year, and vacancy rates remain under 1% in some cities, driving yields higher.

Strong migration

Net overseas migration is strong, but new housing approvals remain 25% below their decade average.

No change in interest rates

Interest rates remain at 3.85%, with potential cuts forecasted later in 2025 if inflation continues to ease.

Investor finance is picking up

Investor finance is picking up, particularly in smaller capitals with rising rents and strong fundamentals.

High-growth opportunities in Perth and Brisbane

Opportunities lie in high-growth, undersupplied areas, predominantly middle and outer-ring suburbs in Perth and Brisbane.

Market Trends

Australia’s housing market is entering a more mature phase of the cycle, one defined by stability, selectivity, and structural imbalance. Growth has become increasingly regionalised, with smaller capitals like Perth, Adelaide, and Brisbane outperforming the larger East Coast cities.

This reflects broader shifts in affordability, the ongoing undersupply of housing, and high levels of population growth in more affordable urban centres. Investor sentiment is cautiously improving, supported by rising rental yields and expectations of interest rate cuts later in the year.

Meanwhile, demand continues to outstrip supply, particularly in rental markets, where tight vacancy rates are fuelling sustained price pressure. The net result is a property market that’s not booming, but still quietly trending upwards in the right places.

A Market Moving in Slow Motion – But Still Moving

Australia’s property market is still creeping higher, just without the fanfare. National home values rose by 0.7% in June, the tenth straight month of growth. It’s not a boom, but it is a consistent climb, and in a high-rate environment, that’s impressive.

Perth remains the clear frontrunner, notching up another 2.0% monthly gain, with Adelaide (1.7%) and Brisbane (1.2%) not far behind. These are markets where affordability is better, rental conditions are tight, and demand continues to outpace supply.

Meanwhile, Sydney and Melbourne barely moved, and Canberra, Hobart and Darwin saw slight declines, a sign that performance is becoming increasingly localised.

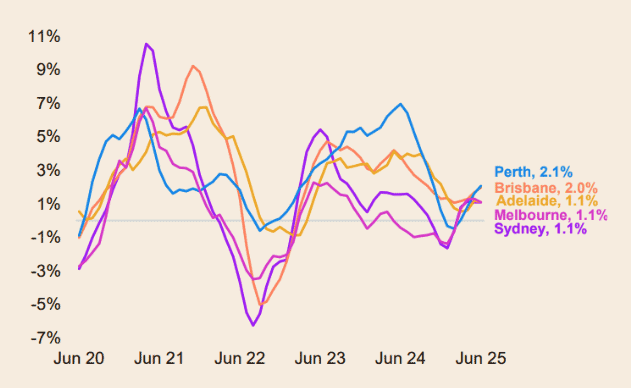

Perth and Brisbane Pull Ahead as East Coast Markets Plateau

The latest rolling three-month change in dwelling values shows that Perth and Brisbane continue to outperform the rest of the country, posting gains of 2.1% and 2.0%, respectively.

These two markets have maintained a clear growth lead through mid-2025, while Sydney, Melbourne and Adelaide all recorded more modest rises of just 1.1%. The divergence highlights the growing gap between markets with affordability tailwinds and those constrained by higher prices and weaker sentiment. After years of relative underperformance, the smaller capitals are now driving national momentum and show little sign of slowing.

Rolling three-month change in dwelling values – State Capitals

Cotality, 2025

Rental growth slows – but remains strong

National rents are up 8.5% year-on-year, with unit rents (+10.0%) still rising faster than houses. While that pace is slower than it was during the 2022–23 surge, vacancy rates remain exceptionally low, keeping upward pressure on rents. In fact, vacancy rates are below 1% in cities like Perth and Adelaide, giving landlords the upper hand.

Yields continue to improve as well. The national gross rental yield is now 3.56%, up from 3.48% a year ago. That’s good news for investors, especially in an environment where capital growth is steady but unspectacular.

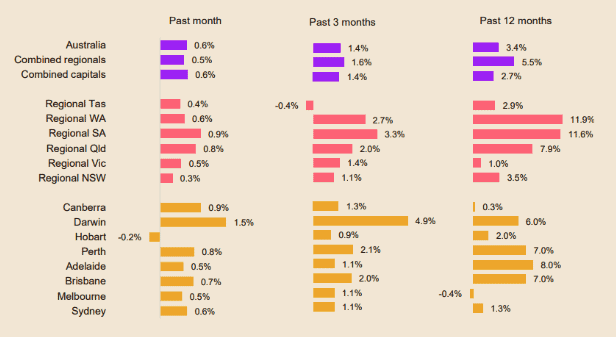

Regionals Lead Annual Growth as Smaller Capitals Stay Strong

Dwelling value growth to the end of June 2025 shows regional markets leading the charge over the past 12 months, with Regional SA (11.9%), Regional WA (11.6%), and Regional Qld (7.9%) all outperforming the national average of 3.4%.

Among the capitals, Adelaide (8.0%), Brisbane (7.0%), and Perth (7.0%) continue to shine, driven by strong fundamentals and persistent supply shortages. Over the most recent quarter, Perth tops the chart with 2.1% growth, followed by Regional SA (3.3%) and Regional WA (2.7%).

The monthly data suggest that momentum remains most consistent in these same regions, while markets like Melbourne (-0.4% over 12 months) and Hobart (-0.2% monthly) continue to lag. The resilience of regional Australia and mid-tier capitals is defining the 2025 property landscape.

Change in dwelling values to end of June 2025

Cotality, 2025

Migration is strong, but housing approvals are still weak

The structural imbalance at the heart of this market hasn’t changed: demand is high, but supply isn’t keeping up. Net overseas migration remains elevated, adding pressure to both the rental and ownership markets. But building approvals are still around 25% below their decade average. Completions are sluggish. And new project launches remain cautious.

Until that changes, undersupplied cities like Perth, Brisbane and Adelaide will likely keep rising. Even with affordability tightening in those markets, the fundamentals are still supportive of further growth.

Interest rates steady… for now

The RBA has now held the cash rate at 4.35% since late 2024. That stability has helped restore some confidence, but a change in direction may still be some time off.

Markets are pricing in one or two rate cuts later in 2025, depending on inflation and wages data. The RBA, for now, is staying hawkish — but cracks are emerging. Consumer sentiment is low, household spending is softening, and unemployment is starting to edge up.

For property, that means we’re in a holding pattern — but potentially at the turning point. If rates do come down, demand will lift. Until then, expect modest, patchy growth.

Momentum builds in smaller capitals

Investors are returning, but they’re being selective. Smaller capitals like Perth and Brisbane are attracting the bulk of investor interest, and for good reason: tight rental markets, improving yields, and still-strong price growth. Investor lending is now growing faster than owner-occupier finance in these cities.

Affordability is also playing a role. As Sydney and Melbourne buyers are priced out, demand is shifting to markets where their dollars stretch further. The momentum may be slow, but it’s starting to build.

What should investors do?

This is a market where smart investors are moving early.

With supply short and demand steady, rents are rising, yields are improving, and capital growth is still on the table, particularly in undersupplied, high-growth cities.

Key strategies for investors right now:

- Follow the supply squeeze, Cities like Perth, Brisbane and Adelaide have some of the lowest vacancy rates in the country

- Target affordability corridors, look beyond the CBD and into the middle and outer rings, where value and rental demand intersect

- Get in ahead of the next rate move. If cuts arrive later this year, competition could intensify quickly.

It’s not a uniform market, but there are clear opportunities for those who know where to look.