Market Trends

April 2026 Market Smart:

The Headlines Say Caution. The Data Says Something Different.

If you’ve been reading the news lately, you’d be forgiven for thinking the property market is on its knees. It isn’t. Yes, Sydney and Melbourne have softened – three rate hikes will do that. But Perth is up over 24% in the past year, Brisbane is the strongest performing capital in the country, and regional markets are quietly outrunning the combined capitals.

Meanwhile, professional investor research tracked by HtAG Analytics is pointing at suburbs that barely register on most people’s radar yet. The broader story of 2026 isn’t one of caution – it’s one of opportunity hiding in plain sight. And as always, the people who find it first are the ones who were already looking.

Key Take Aways

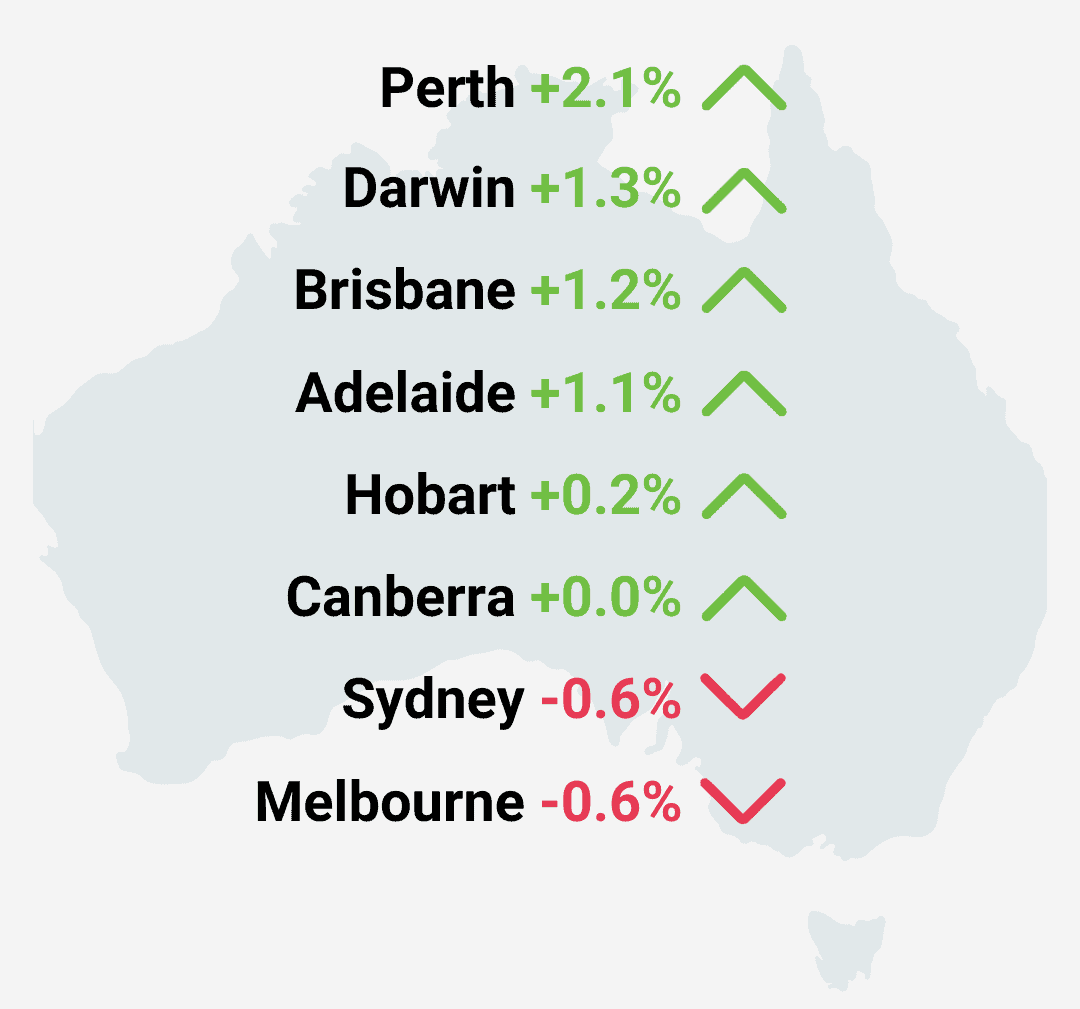

Most of the country is still growing - strongly.

Sydney and Melbourne softened in April. Perth, Brisbane, Adelaide, Darwin, and most regional markets didn’t.

Rate hikes create negotiating room that rarely lasts long.

The cash rate is at 4.35%, and conditions in some markets have eased. Prepared buyers with good pre-approval are in a stronger position than they’ve been in years.

Brisbane leads the country at 19.6% annual growth – with more to come.

Queensland’s supply-demand imbalance isn’t resolving quickly. ANZ forecasts another 9.7% this calendar year, and the Olympic pipeline is a genuine long-run tailwind.

HtAG data is flagging suburbs most investors haven't noticed yet.

Sunbury (RCS 91), Calwell ACT (RCS 91), Madeley WA (RCS 90), and Northcote units (RCS 94) are the current standouts – strong fundamentals, still-accessible prices.

Rental income is re-accelerating. Vacancy is 1.6% nationally.

Darwin leads at 9.2% annual growth. Perth and Brisbane follow at 6.7%. The case for rental property investment is as strong as it’s been in years.

History favours buyers who act in low-confidence periods.

The investors who’ll look back on 2026 as a turning point are the ones doing their research and moving with conviction – not waiting for a certainty that rarely comes.

What’s Moving and What Isn’t

The Cotality’s April 2026 Home Value Index 0.3% sounds underwhelming until you realise that Sydney and Melbourne are largely responsible for dragging it down. Both cities fell 0.6% for the month. Strip them out, and the picture brightens considerably.

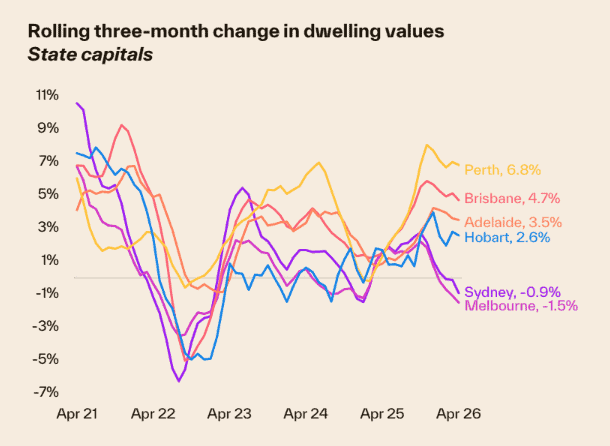

Perth is up 24.3% year-to-date. Brisbane delivered 19.6% annually, the strongest result of any capital, and Adelaide values have risen more than 90% since 2020. The national median is $933,137, with annual growth running at 9.9%, and even within Sydney, lower-quartile houses rose 0.8% while the top end fell 0.9%. The demand is there. It’s just concentrating on where prices still make sense.

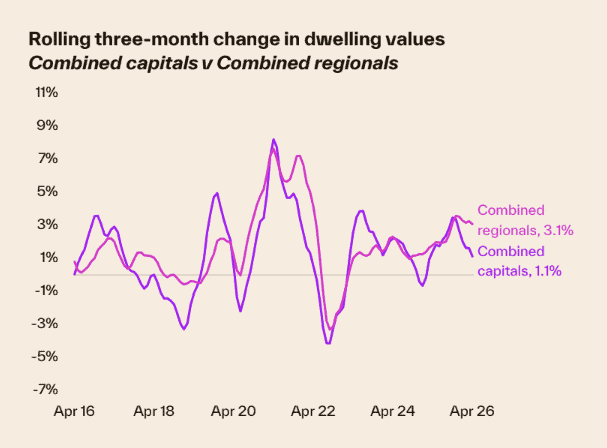

Regional markets are becoming a genuine story in their own right this year, up 3.3% for the March quarter, compared with 1.8% across the combined capitals. Regional WA is out in front, but Queensland, SA, and parts of Victoria are all running hard. For investors open to looking a little further afield, the numbers are hard to ignore.

Cotality 2026

How Buyers and Sellers Are Feeling Right Now

Consumer confidence is subdued, the ANZ–Roy Morgan index sits at 67.2, well below neutral, and three rate hikes have pushed the cash rate to 4.35%. Mortgage stress is real for a meaningful share of borrowers, and that needs to be factored into any cashflow analysis. We’re not dismissing that.

What history tells us, though, is that periods like this tend to create some of the best entry conditions available to prepared buyers. Auction clearance rates in Sydney and Melbourne are below average, listings are rising, and sellers are negotiating in ways they simply weren’t six months ago. More choice, less competition, and more room to move all add up to a buyer’s environment.

In Brisbane and Perth, the market remains firmly in the seller’s favour, with well-presented properties still selling quickly and drawing genuine competition. Two very different sets of conditions, both with merit for investors, depending on your strategy.

Cotality 2026

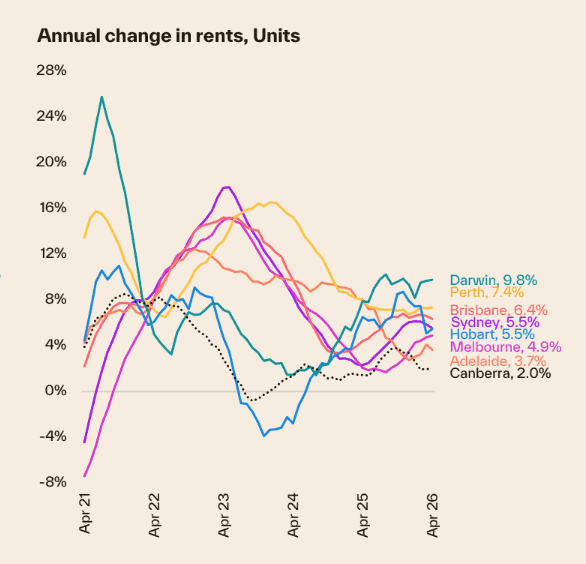

Rents Are Moving Again, and They’re Not Slowing Down

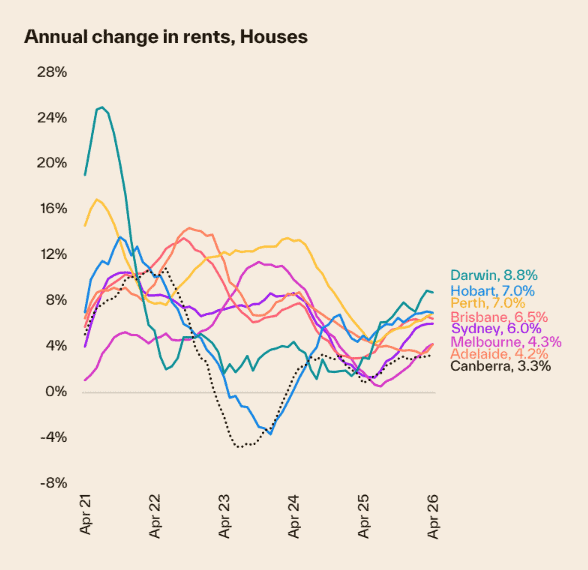

After a mid-2025 easing, the rental market has re-accelerated sharply, and for property investors, that’s an important development. Cotality’s Q1 2026 Rental Review shows national rents rising 2.1% over the March quarter, up from 0.9% in Q3 2025. In annual terms, rents are now 5.7% higher than a year ago.

Darwin leads all capitals with 9.2% annual rental growth, reaching $699 per week. Perth and Brisbane follow at 6.7% each, both markets where high rental income sits alongside strong capital growth. Sydney’s median rent has hit $824 per week, up 5.9% year-on-year. Melbourne, at 4.4% annual growth, is the slowest mainland market but is re-accelerating from a low base.

The national vacancy rate is just 1.6%, and in Queensland it’s 1.0% statewide. With new dwelling completions running well below what population growth demands, this is a structural story, not a cyclical one. For investors, that means the rental income case for well-located property is as compelling as it’s been in years.

Cotality 2026

What the Professional Investor Data Is Telling Us

While sentiment surveys paint a bleak picture, professional investors’ behaviour tells a different story. HtAG Analytics tracks suburb-level fundamentals across thousands of active investors and buyers’ agents, and the data currently points to some markets that aren’t on most people’s radar.

Victoria is dominating capital growth searches in the mid-budget range, and a couple of names keep coming up. Sunbury is scoring 91 out of 100 on HtAG’s Relative Composite Score, with 12% annual growth, and it’s appearing across both mid- and upper-budget searches, which tells you something about the depth of demand there.

Doreen is another consistent performer with a Relative Composite Score of 80, 11.2% growth, and a vacancy rate of just 1.3%. In South Australia, Lightsview and Mawson Lakes are both strong with scores of 78 and 66 respectively. Frenchville in Rockhampton might not be on many investors’ radars, but it probably should be. HtAG is showing 17.8% annual growth, an RCS of 74, and a median price of $681,000 – the kind of numbers that are simply out of reach in most metro markets right now.

For investors with yield front of mind, Wembley in WA is the standout with a Relative Composite Score of 87, gross yield of 5.4%, and 20%-plus annual price growth. That combination doesn’t come around often. And for cashflow closer to home, Melbourne’s inner-north unit market is quietly delivering. Northcote is scoring a Relative Composite Score of 94 and Brunswick at 89, with gross yields running between 5.5% and 6.3%. Strong returns in a segment that often gets overlooked.

Things to Keep an Eye On

RBA rate trajectory. The cash rate is now 4.35%, and markets are pricing one more hike. The good news: every time the RBA signals it’s finished, buyer demand has historically returned quickly. Positioning ahead of that moment is where the opportunity sits.

APRA’s DTI lending cap. Investor credit growth is running at its fastest pace since 2015 – a sign of genuine market conviction. Worth monitoring in case further tightening affects access for leveraged buyers.

Consumer confidence recovery. At 67.2, confidence is near historic lows – which also means the upside from here is significant. When sentiment turns, it tends to move fast. Growth corridors in Melbourne and Sydney are likely to be among the first to feel it.

Brisbane’s Olympic infrastructure pipeline. Planning approvals and rezoning decisions tied to 2032 are creating real, long-term value in inner and middle-ring Brisbane. This is a multi-year tailwind that’s still in its early stages.

Regional vacancy and rent momentum. Combined regional vacancy is 1.9% with rents growing 6.0% annually. Markets like Toowoomba, Ballarat, Bendigo, and Bunbury offer strong fundamentals at price points that are still genuinely accessible.

The supply gap. A long-run tailwind for investors. Just 168,050 dwellings commenced nationally in 2024, well below demand. Until that changes materially, the structural conditions supporting both price growth and rental income remain firmly intact.