- The first step is making the call.

- 1300 022 482

- hello@searchpartyproperty.com.au

31st October 2023 – Property Market Update

Record Market Fast Approaching

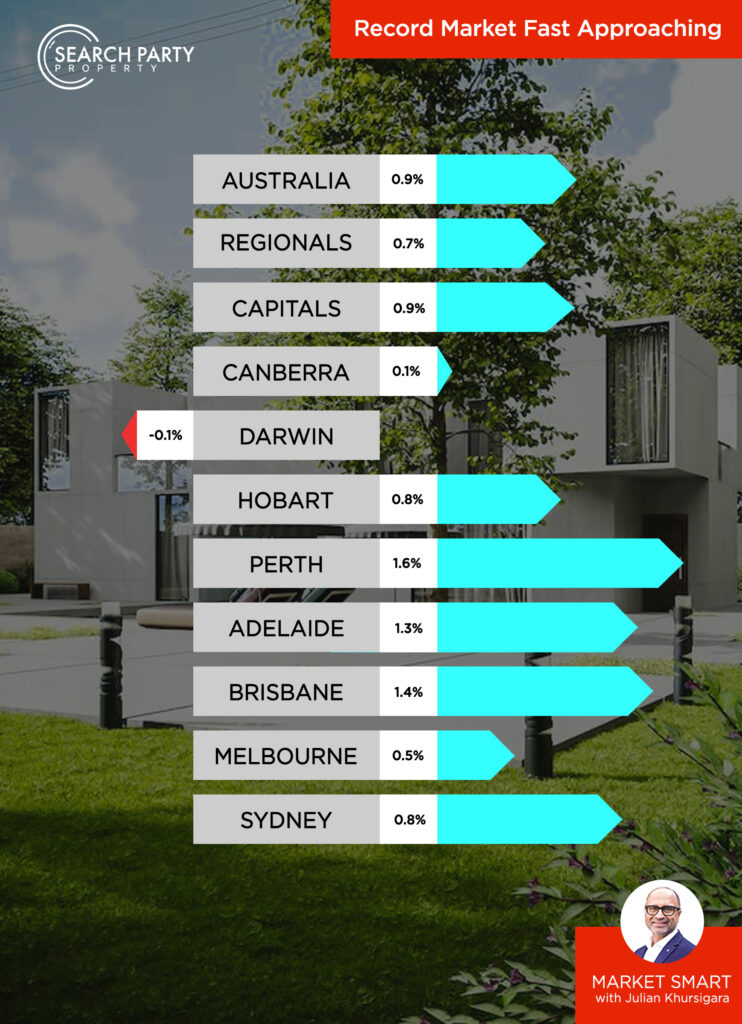

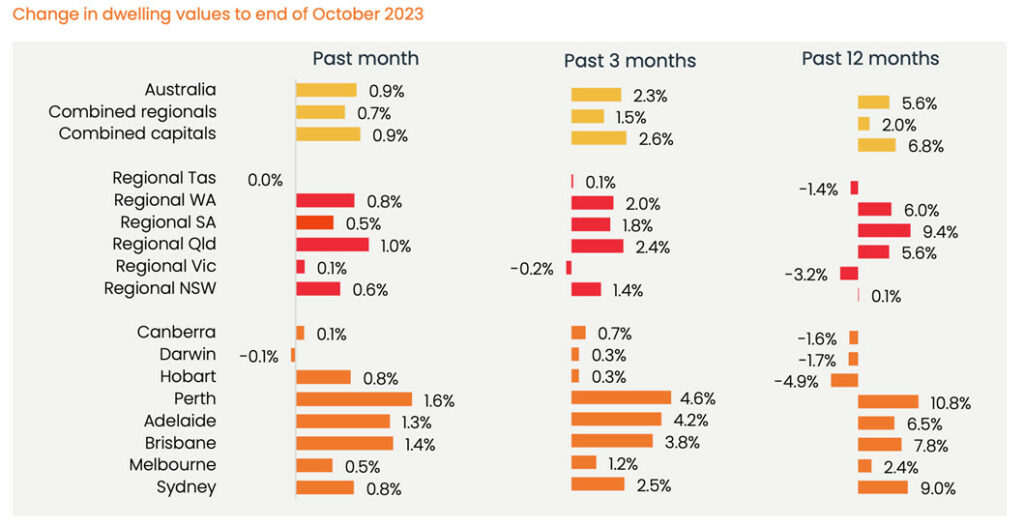

The Australian property market is in a pivotal phase, poised to hit unprecedented new heights. CoreLogic’s Home Value Index indicates a 0.9% price rise for October, contributing to an overall 7.6% increase since January – with the market now just half a percent below last year’s record high for aggregate national values. However, with a further rate rise on the cards and a slowing rate of growth, questions remain concerning the ongoing resilience of this trend.

Where we are now?

Since early this year, the market’s trajectory has taken on a consistent pattern. National home values have not only rebounded from the January trough but produced consistent energy. Capital cities are leading the charge, with Perth, Brisbane, and Adelaide showing remarkable year-to-date performance. Brisbane, in particular, has seen a notable rebound, erasing the previous downturn to reach new heights. The market’s momentum is not uniform however – while Darwin has seen a marginal contraction, Sydney and Melbourne remain below peak levels, suggesting room for growth or a recalibration of values in these markets.

Regional markets, typically trailing their metropolitan counterparts, have also shown signs of uplift, albeit at a more measured pace. This is indicative of a broader, holistic growth across the nation, albeit with an understanding that such growth is not without geographic idiosyncrasies.

How did we get here?

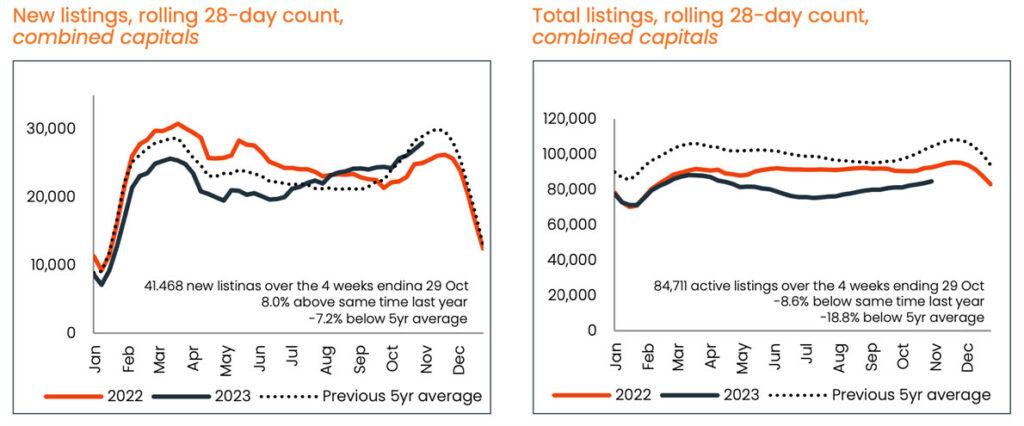

The latter part of the year has seen a distinct uptick in the number of new listings in capital cities. The flow of new listings through the winter and spring months has been robust, standing nearly 12% higher than the previous year. This resurgence of vendor activity has introduced more options for buyers and is a clear shift from the below-average activity noted over the past 10 months.

While there has been an increase in new listings, the cumulative total listings (including both new and re-listings) are still trailing behind last year’s figures and are below the five-year average. Despite this, there’s an unmistakable rise in inventory levels, with CoreLogic’s data showing a 5.1% increase in total capital city stock since the onset of spring. This trend is indicative of a market where buyer demand is not matching the surge in new listings.

Across the major cities, Perth has seen its advertised stock levels diminish through spring, with a decrease of 2.1% from the end of winter. Brisbane and Adelaide have experienced marginal changes, with listings barely increasing. In contrast, the ACT has seen a significant jump in total listings of 21.3% through spring to date. Melbourne and Sydney have also experienced an uptick in listings by 10.7% and 9.3%, respectively. Hobart’s listings have remained well above average for an extended period.

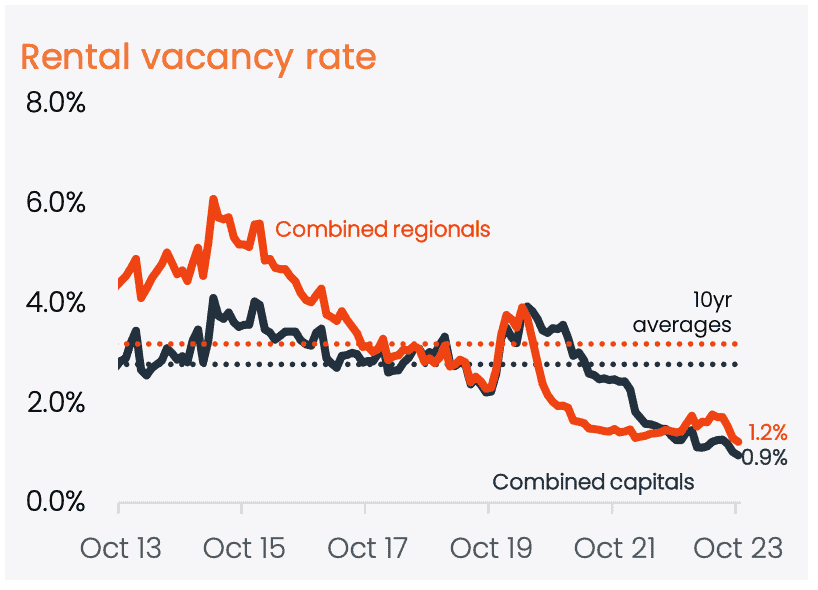

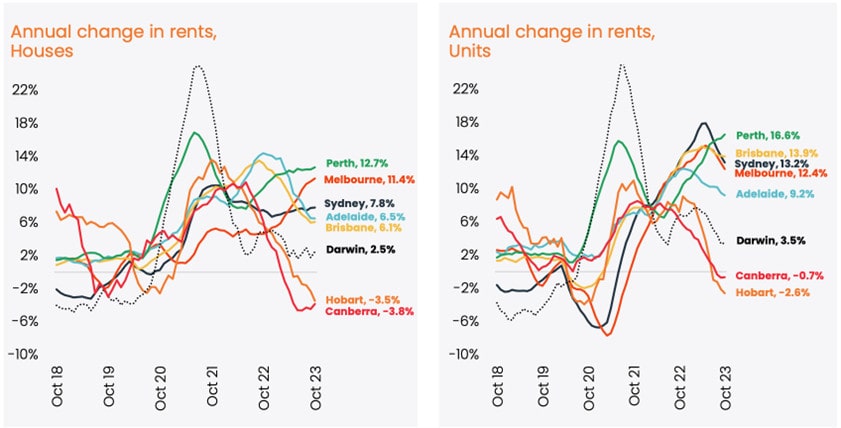

Interestingly, October marked a historic low in rental vacancies, with a mere 0.9% in the capitals and 1.2% regionally. National listings were strikingly scarce, 35.5% below the five-year average and 16.1% less than the prior year. The rental market has yet to exhibit a supply response, with listings on a continual decline and rents rising for a 39th consecutive month.

Although the rental growth pace has moderated, particularly in the unit sector, it remains diverse, with the quarterly growth rate in the capitals tapering from 3.1% to 1.8%. The disparity between house and unit rents is growing in cities like Sydney and Melbourne, potentially linked to the academic year’s influence on foreign student housing demand. Perth stands out for its significant annual rental increases, while markets such as Hobart and Canberra experience rent reductions correlating with more average vacancy rates. As property values ascend and rental growth slows, gross rental yields that peaked nationally at 3.73% have slightly receded to 3.69% in October.

Where are we going?

Though it looks all but certain that the market will reach a new national value record later this month, here are a few things that may be worth keeping an eye on, as the expected growth continues to play out.

Interest Rates

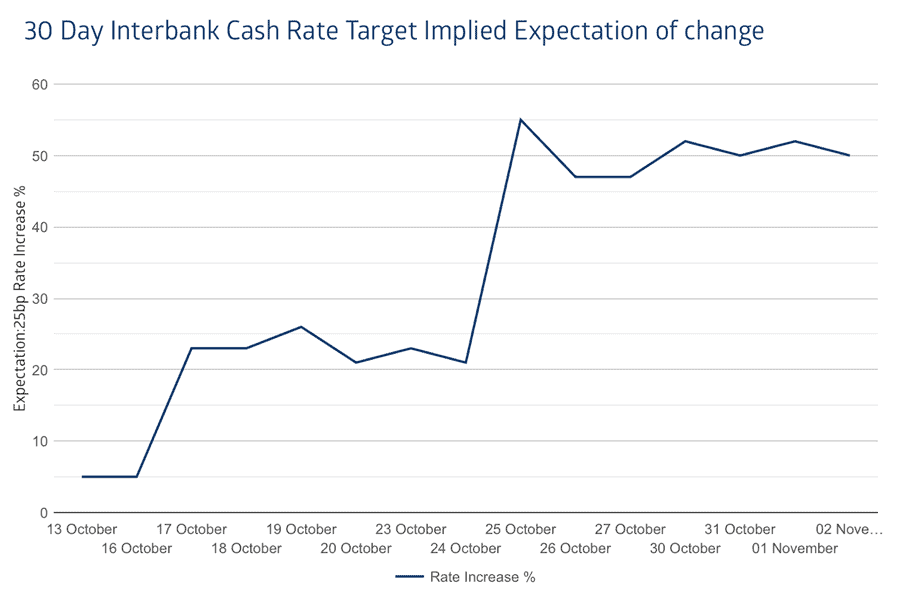

Market consensus is beginning to coalesce around the RBA announcing a 25-basis point rate hike on Cup Day – currently priced in at around a 50% probability. This would mark the RBA’s 13th consecutive rate increase, though, most expectations suggest that this would likely be the peak of interest rates before they begin to ratchet back down into 2024. Yet again, it seems that interest rates aren’t having a fantastic impact upon inflation – as we suggested some months ago.

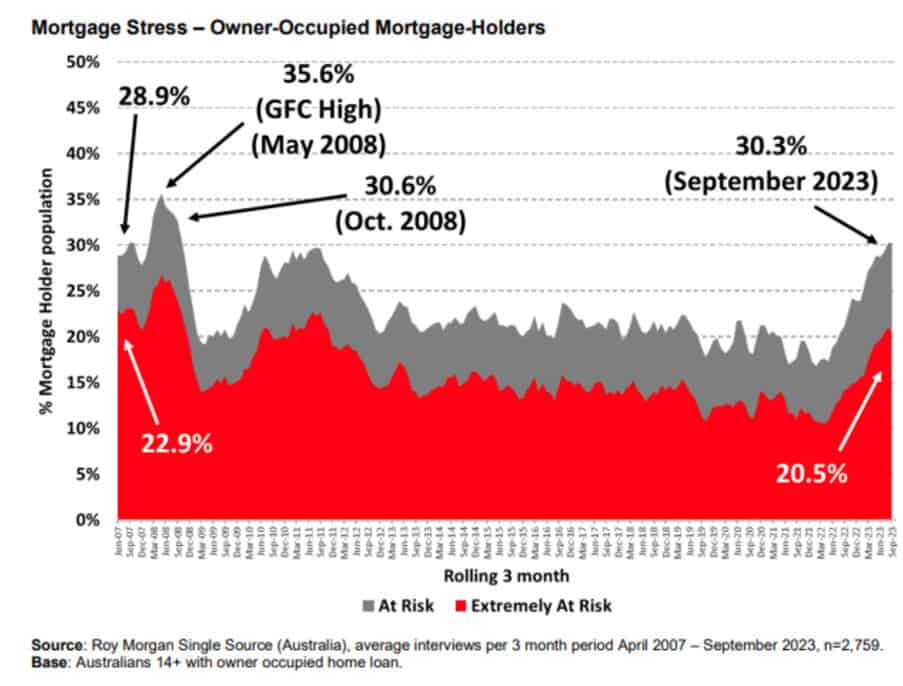

With this hike expectation, also comes the reality of added mortgage stress. According to a Roy Morgan survey, September saw the highest rates of mortgage stress since 2008 – when the cash rate was way up at 7.25%.

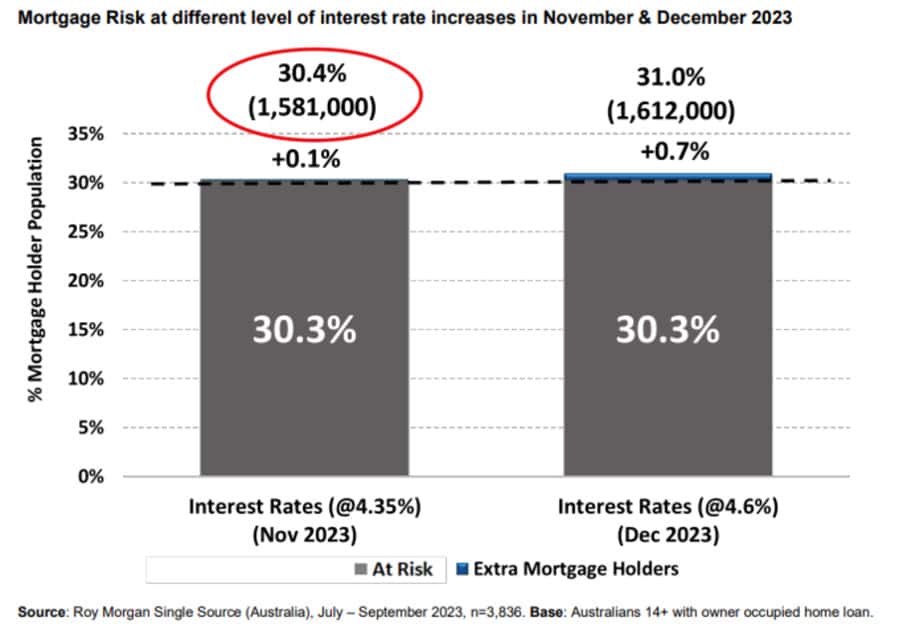

Roy Morgan has also assessed the conservative impact of potential rate rises in November and December, indicating the knock-on effects for mortgage stress levels:

Mortgage Financing

The ABS notes a significant increase in mortgage refinances over the past three years, hitting a peak of $21 billion in mid-2023. The recent slowdown to $18.5 billion in September suggests the ‘refinancing boom’ is losing steam, aligning with the end of fixed-rate mortgage terms from the pandemic era. Households are already allocating a record portion of income to debt repayments, a burden that will only grow if interest rates rise further. Though prices continue to rise, it seems that investors are increasingly unable to capitalise due to costs – as is reflected among the investment trends.

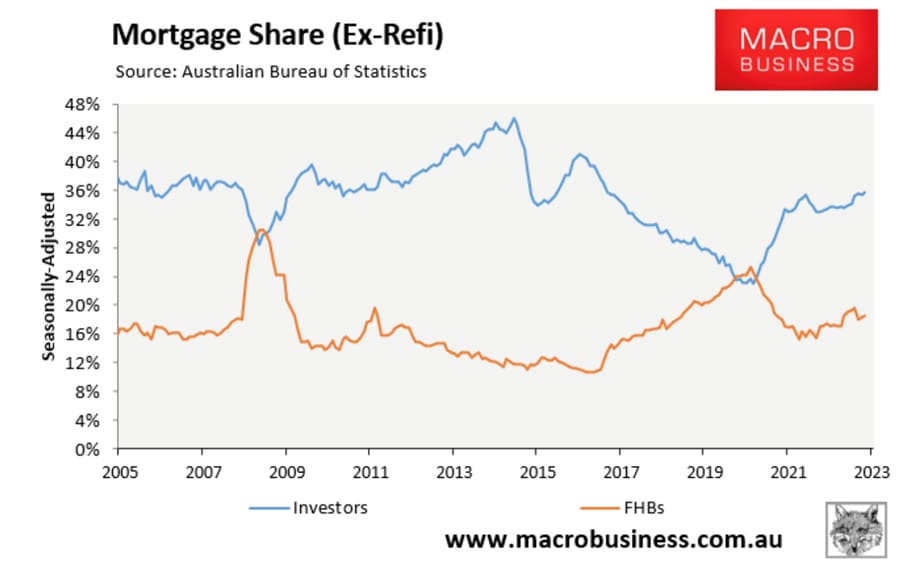

Investor Trends

The investor landscape is witnessing significant churn. On the one hand, there’s a notable exit of investors from the market, impacting rental supply and contributing to the tightening of rental vacancy rates, which are at a record low of 0.9%. On the other hand, new investor lending is on the rise, with a 2.0% increase in September and a 2.6% year-on-year growth, indicating a vibrant entry of new investors into the market. This shift suggests that while some are seizing the opportunity to realise gains, others are entering in anticipation of future growth, especially considering the constrained construction activity and booming population growth.

At Search Party Property, we specialise in developing tailored investment strategies and will work with you to come up with a suitable plan of attack. We also regularly assess your strategy ensuring that it is fit for purpose and delivering the desired results.

{kind=link}

{kind=link}

{kind=link}