- The first step is making the call.

- 1300 022 482

- hello@searchpartyproperty.com.au

29th February 2024 – Property Market Update

February Market Smart – Perth Accelerates!

Key Takeaways

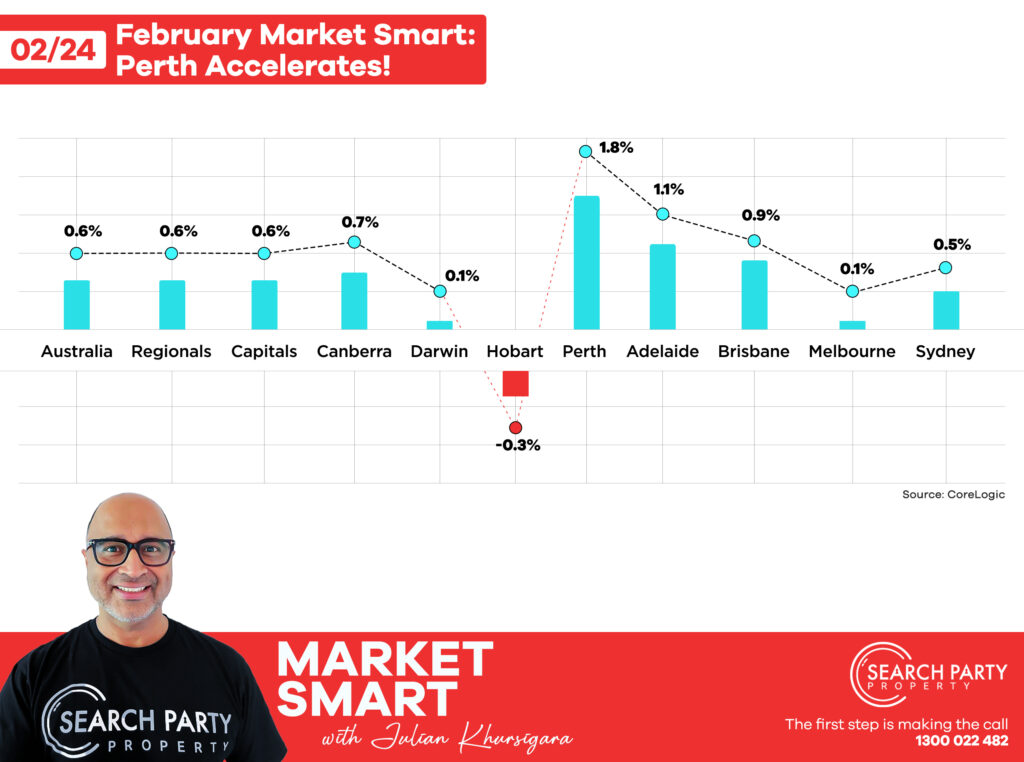

- Perth (1.8%) continues to outpace all other capital cities, and the gap in performance is widening.

- Brisbane (0.9%), Melbourne (0.1%), Sydney (0.5%), Darwin (0.1%), Canberra (0.7%) and Hobart (-0.3%) have all performed better across the past month, though Hobart remains in decline.

- Adelaide is the only city to return stagnant growth figures since January, despite maintaining second fastest monthly rise in house prices (1.1%).

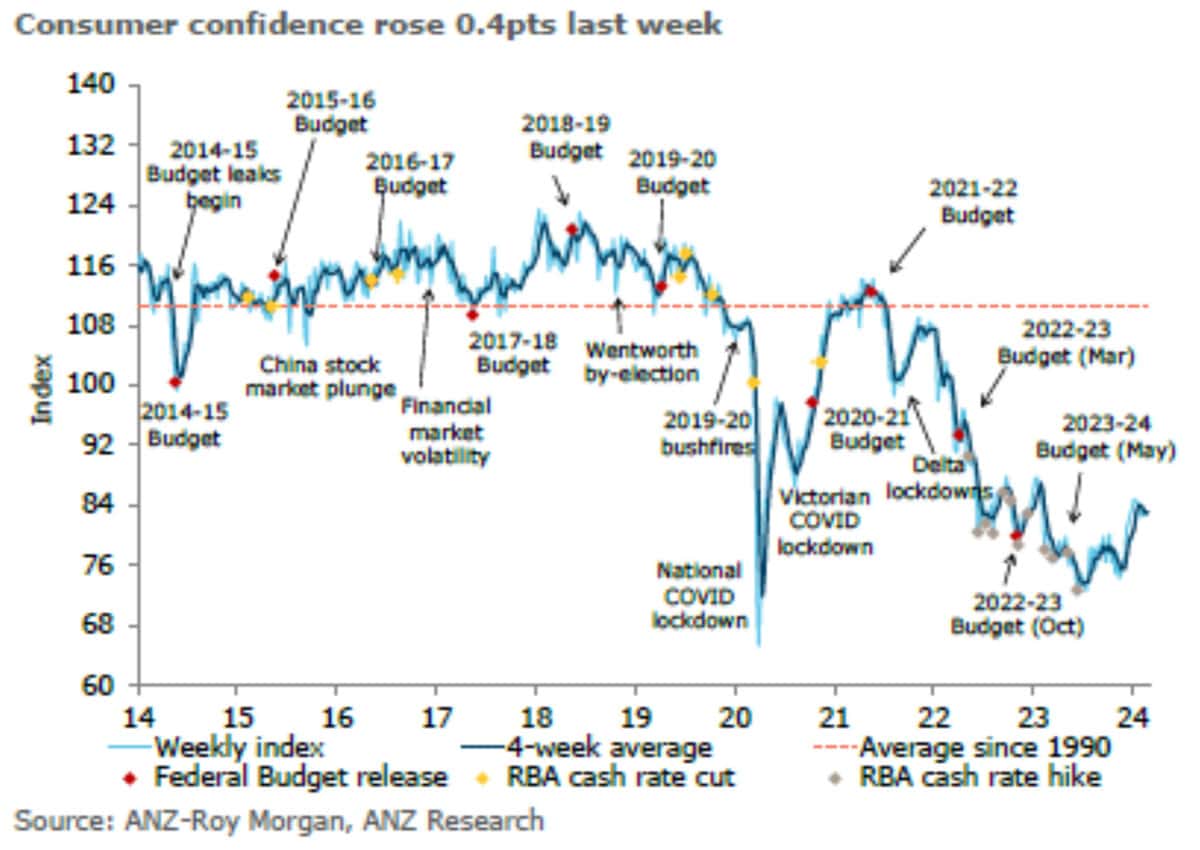

- Consumer confidence, while still pessimistic, is at its highest level since mid-2022. This may amplify the effect of an eventual rate cut upon prices.

Current Market Trends

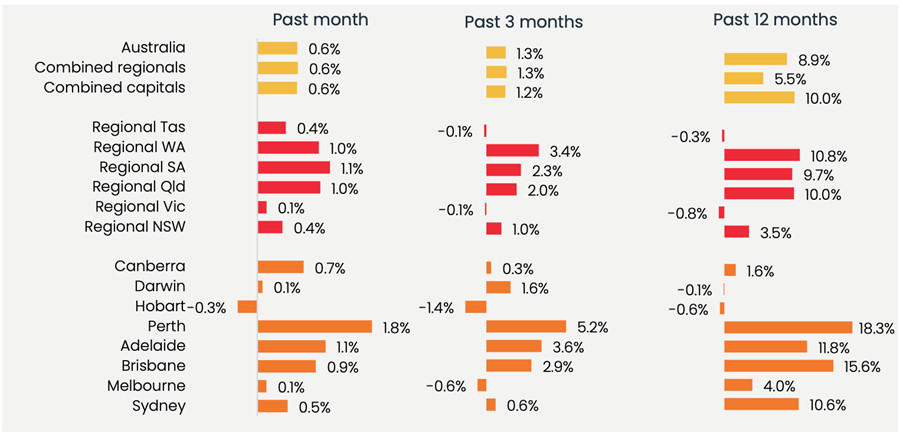

The market continues to display considerable diversity across regions and cities. In the past month, overall growth was at 0.6%, up from 0.4% in January. Perth (1.8%), Adelaide (1.1%), Brisbane (0.9%) and Canberra (0.7%) outpaced this average.

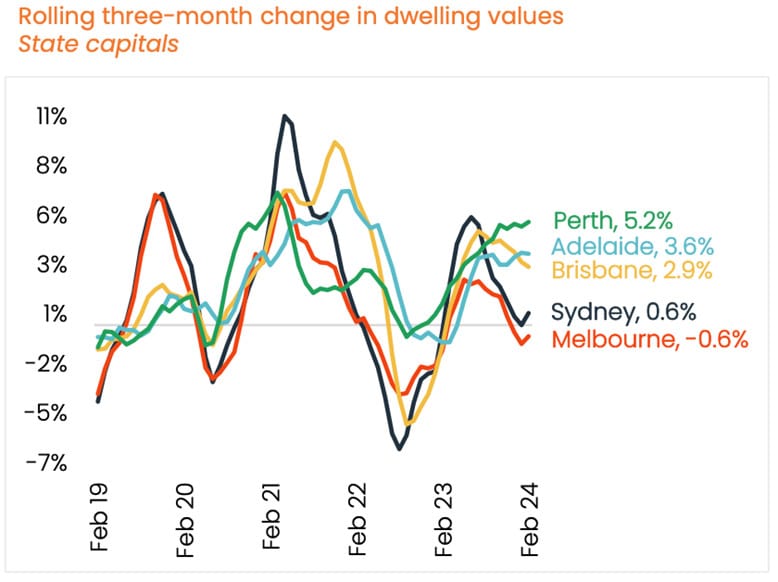

On a rolling three-monthly basis, the broadening gap in house price performance becomes more obvious, with Perth continuing to trend upwards at 5.2%. Of the 5 largest state capitals, Brisbane is currently experiencing the longest quarterly downward trend, now at 2.9%, though remains in third place. With this trend, the lead of breakaway pack (Perth, Adelaide, Brisbane) appears to be diminishing overall.

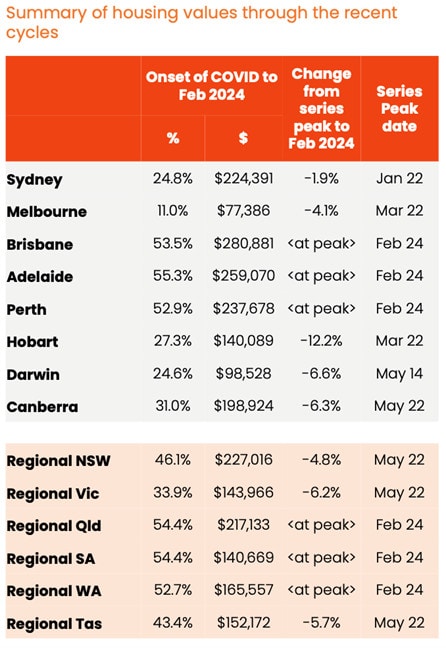

Despite this change, Perth, Adelaide, and Brisbane, along with their respective states, remain the only markets at peak price levels since COVID. Brisbane continues to demonstrate the greatest post-COVID performance in terms of dollar value, while Adelaide has had the most impressive percentage rise.

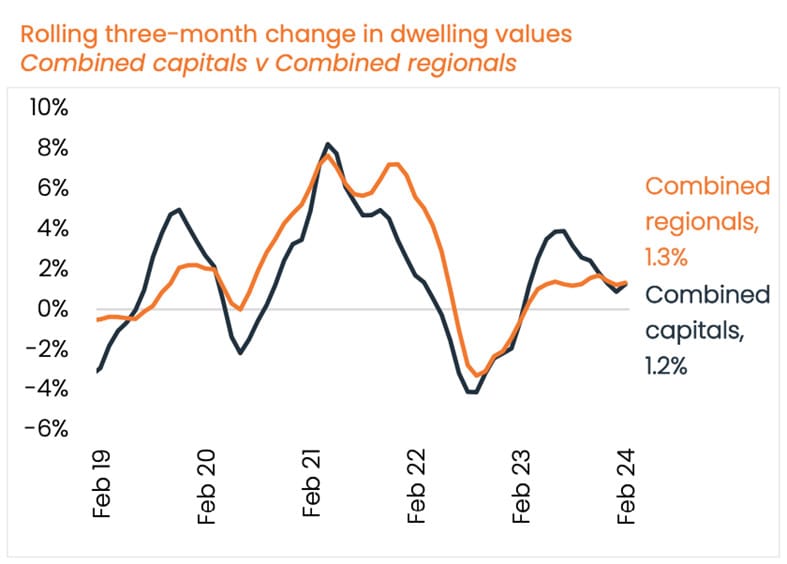

There continues to be strong momentum within regional markets, as quarterly growth among combined regional markets (1.3%) continues to outpace that of the combined capitals (1.2%).

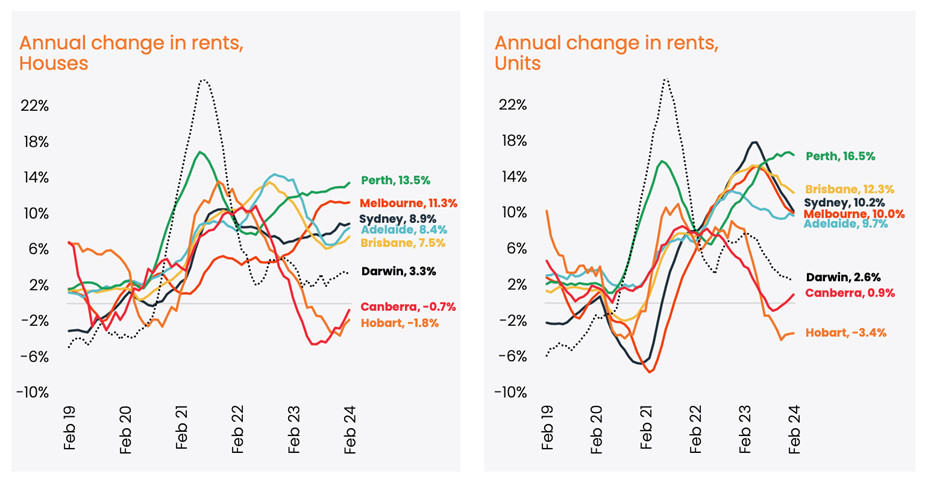

Unfortunately for renters, the pace of rental growth has also quickened to 0.9%, the fastest rate of growth since March 2023. This is a seasonal pattern, with Q1 traditionally exhibiting a faster pace for rental growth. However, rental growth among units has continued to slow since April 2023.

Things to keep an eye on:

- Consumer Confidence

ANZ-Roy Morgan’s consumer confidence index has hit its highest levels since early last year, though remains firmly in pessimistic territory.

Up from its trough in mid-2023, consumer confidence looks to have turned a corner in 2024 with a series of impressive rises. The announced changes to the stage 3 tax cuts seem to have had a buoying effect, as have the growing expectations of an end to the rate hike cycle.

Research tells us that consumer confidence should be considered a ‘lagging’ indicator of economic performance, but it is also said to have an amplifying, rather than a determining effect upon market direction. In other words, if economic indicators have begun to improve, a subsequent rise in consumer confidence will amplify the trend. It’s unlikely that consumer confidence will move in a direction contrary to economic performance.

This also seems to follow from a real estate perspective. Last year saw continued resilience in property markets despite particularly adverse conditions, and with 2024’s continued growth, consumer confidence has begun to take note. If and when rates begin to come back down, growing consumer confidence is likely to magnify the impact of those improved conditions upon price growth.

- Interest Rates

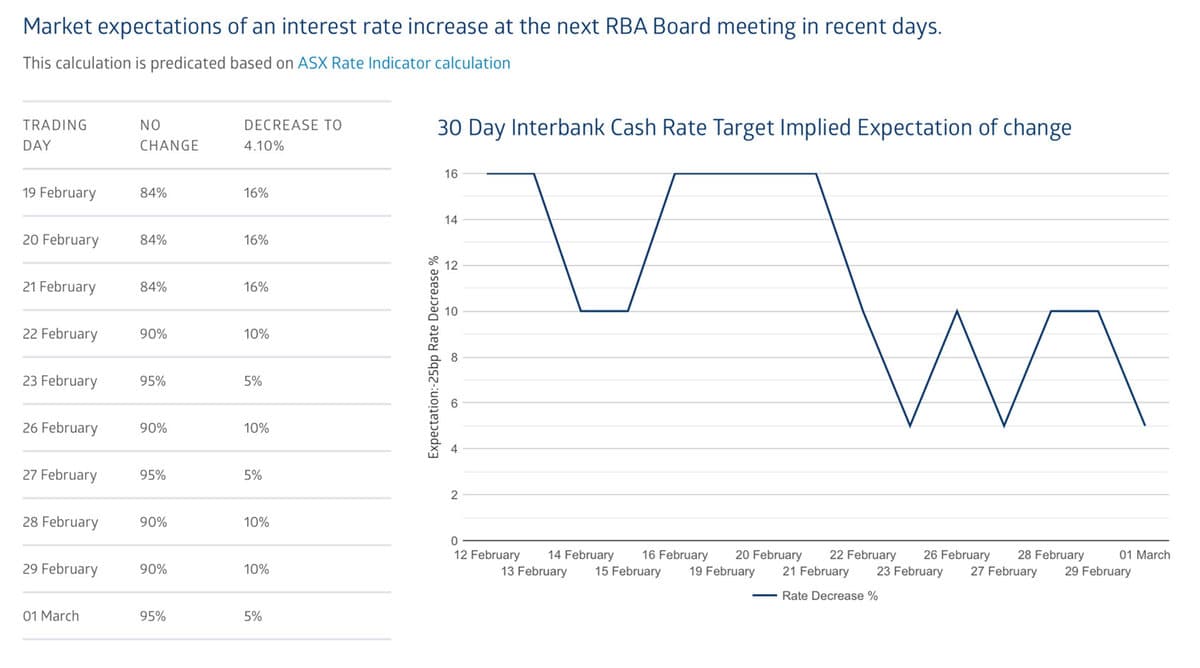

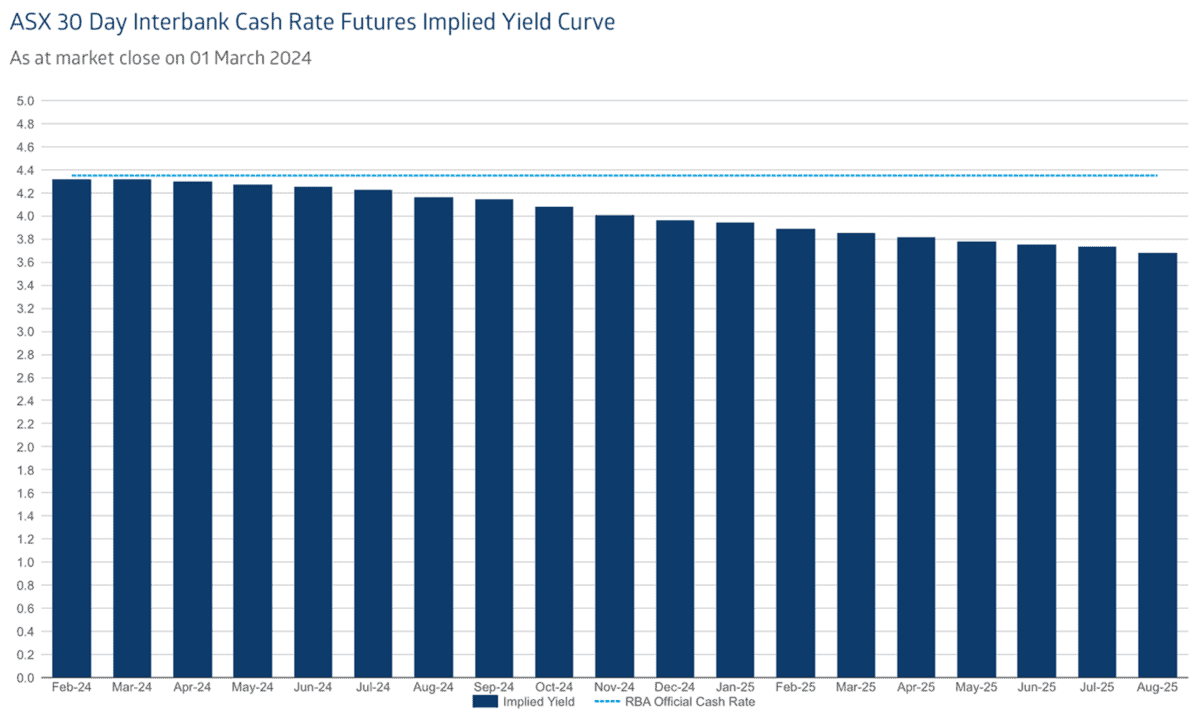

Over the past couple of weeks, expectations of a rate cut announcement in March have continued to fall:

According to futures markets, the first rate cut the latter half of this year, which mirrors CBA and Westpac estimates. ANZ and NAB meanwhile are not expecting cuts until November.

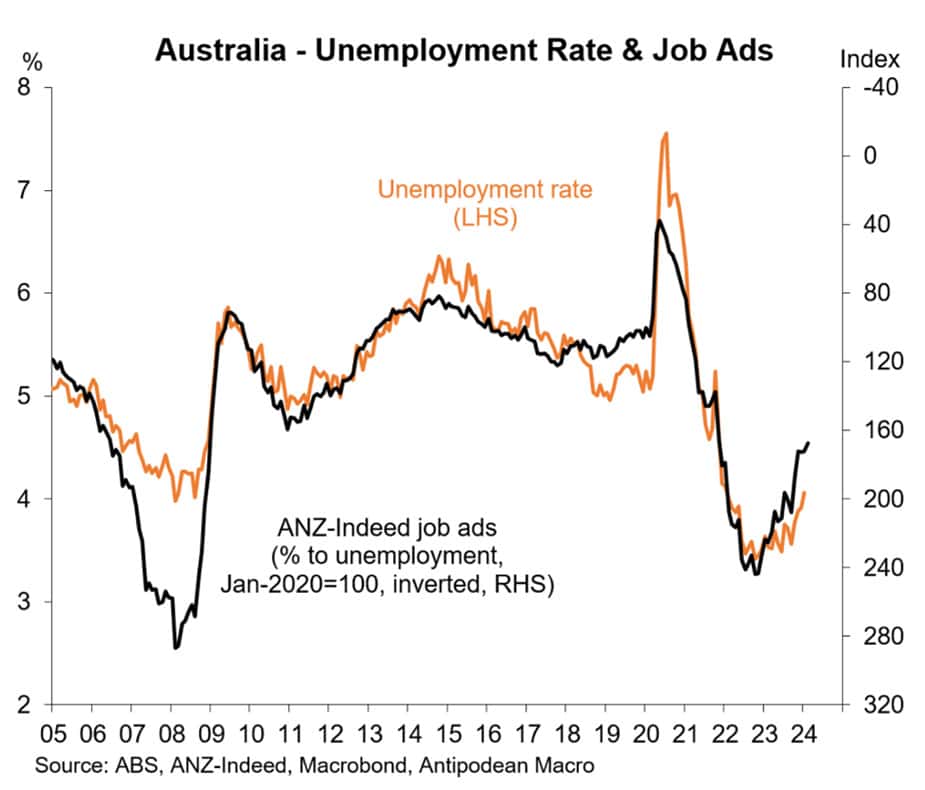

The reasoning for this is multifaceted, but inflation and unemployment figures are of course key. Unemployment has since September risen by 0.5% to 4.1%, the highest level in two years:

Should this continue at such a pace, rate cut expectations could well be brought forward to June or August, as economists at AMP have suggested.

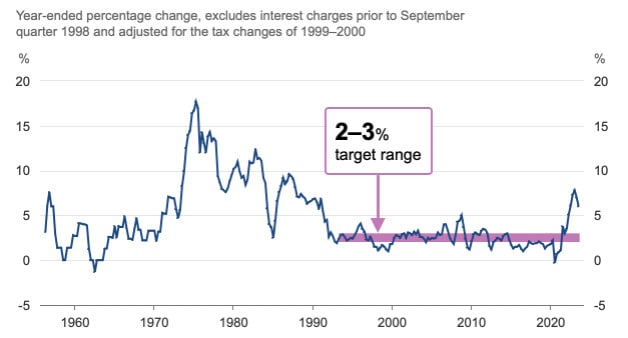

Inflation, the RBA’s other chief concern, has come down rapidly but remains historically high and above target at 4.1%:

- Housing Supply

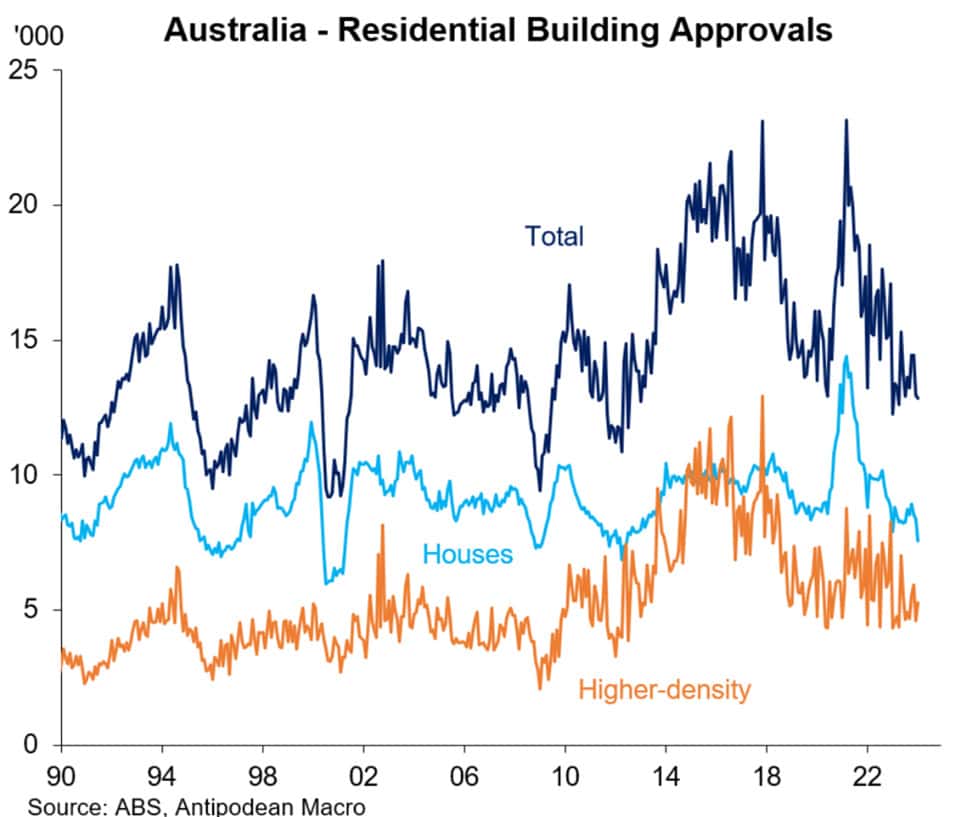

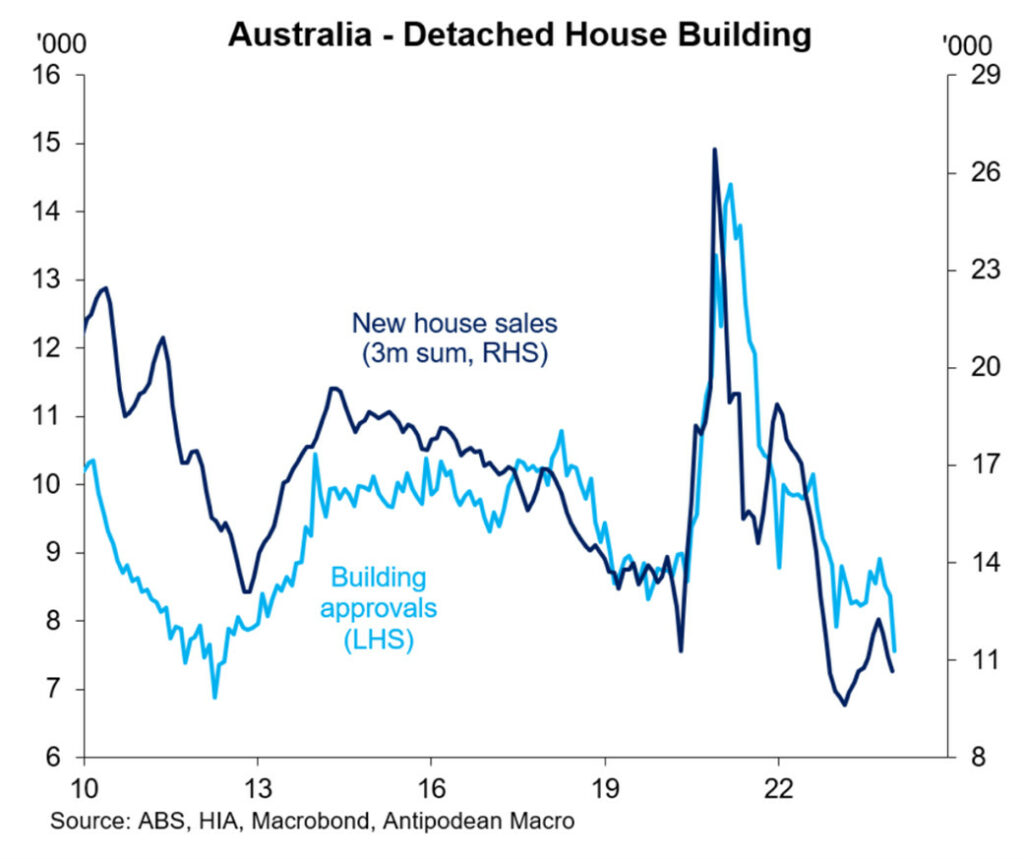

We all know that price action is the result of supply and demand. For real estate, new housing supply can be considered in a variety of ways, and building approvals are one such metric. For both houses and higher-density properties, the rates of approvals are continuing to decline:

Importantly, it seems that this has been foreshadowed by a preceding decline in the number of new home sales, likely associated with currently high financing costs:

With population growth and migration remaining so high, these continued supply trends are set to mean lower vacancy rates and higher rental and price growth for longer

At Search Party Property, we specialise in developing tailored investment strategies and will work with you to come up with a suitable plan of attack. We also regularly assess your strategy ensuring that it is fit for purpose and delivering the desired results.

{kind=link}

{kind=link}