Is Melbourne oversupplied with property?

Like any market, property prices are a consequence of supply and demand.

For many months now, we’ve heard a similar refrain concerning the ‘chronic undersupply’ of housing across the market. Housing Australia has even forecast a national shortfall of 100,000 homes in just four years’ time.

This being true, how is it possible for Melbourne to be oversupplied with property?

Based on CoreLogic figures, Melbourne saw 90,000 total property listings across 2023, alongside just 81,203 total sales.

Furthermore, SQM reports that in January of this year, total listings rose 6.2% above the number of listings a year prior – a surplus of some 32,000 properties. New listings also rose substantially, 21.7% higher than a year prior. This figure was second only to Darwin among capital city property markets.

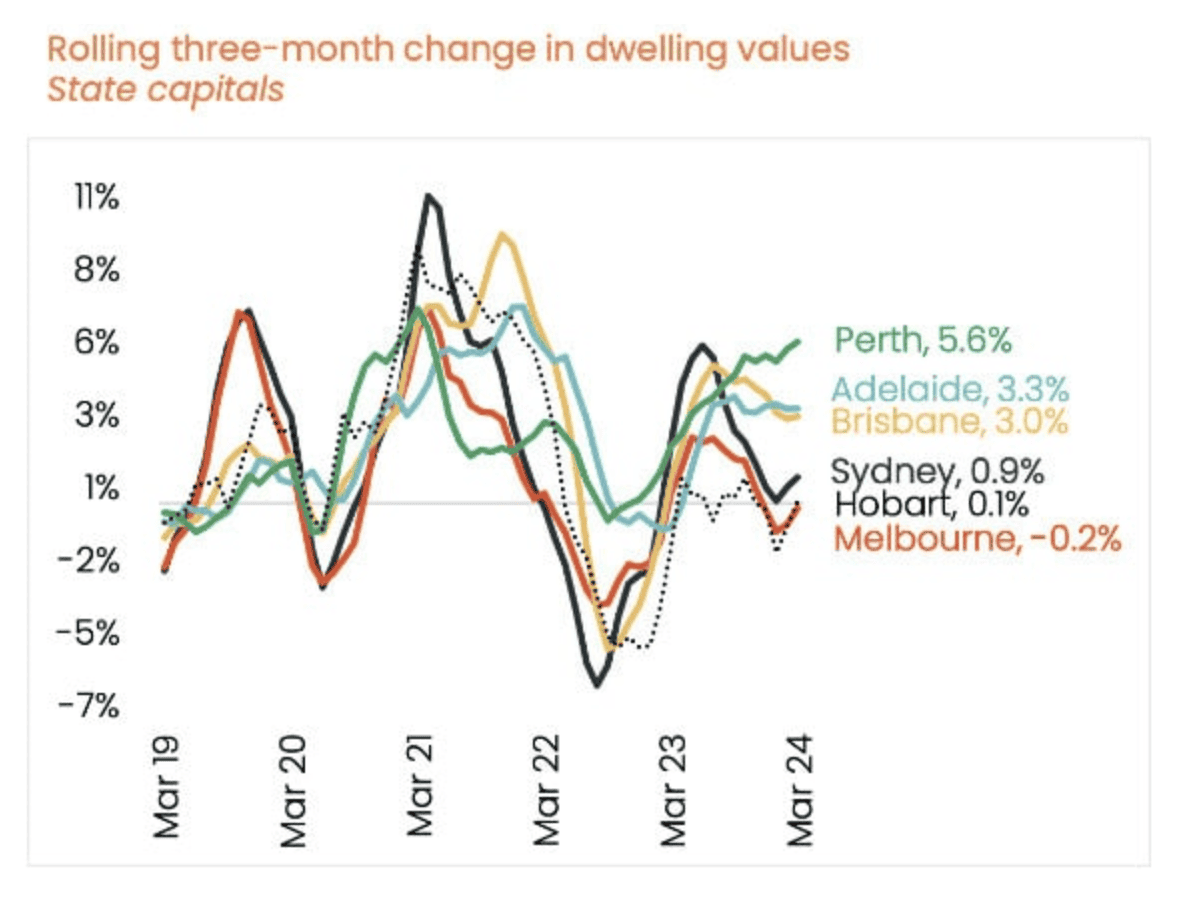

These figures did mean that, throughout 2023, Melbourne property experienced a level of contraction:

The apparent contradiction at play here comes down to a conflation of concepts, particularly concerning demand.

There is a difference between two types of demand within a market.

Some might refer to these as ‘purchasing demand’ vs ‘underlying demand’ – i.e. in this case, the demand for home ownership vs the demand for somewhere to live.

You might also describe this as the difference between the number of prospective buyers who are both interested and capable of purchasing a property, vs the number of buyers who are interested, but not capable of purchasing a property.

This means that, despite record levels of net overseas migration (with Melbourne historically receiving ~30% of overseas arrivals), such rapid population growth isn’t necessarily replicated 1:1 with purchasing demand in the property market.

Though of course, new migrants all need somewhere to live, even if they aren’t in the market to buy a home right now.

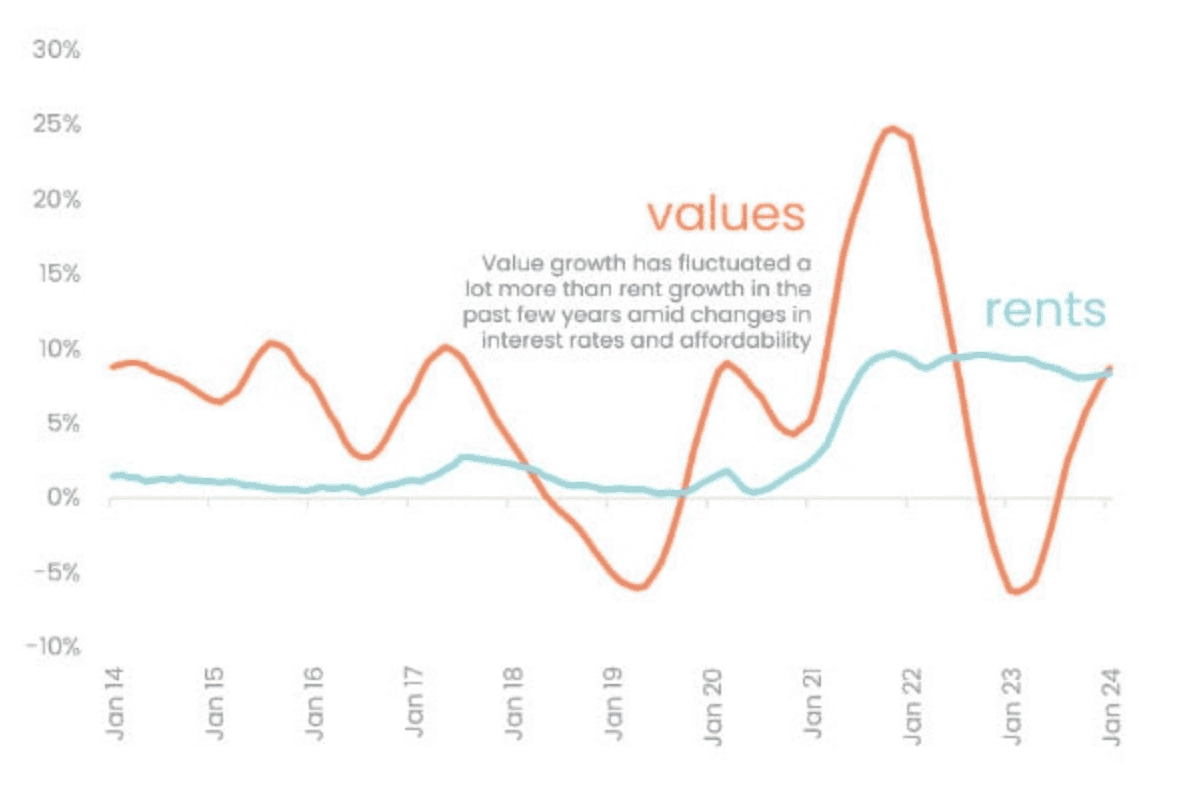

We can observe the effects of this discrepancy within Melbourne’s rental market, compared to the performance of Melbourne house prices:

We can observe the effects of this discrepancy within Melbourne’s rental market, compared to the performance of Melbourne house prices:

Rental growth has remained particularly stable, despite vast fluctuations in home price growth. While the fundamental demand for a place to live is strong, demand for home ownership is weaker.

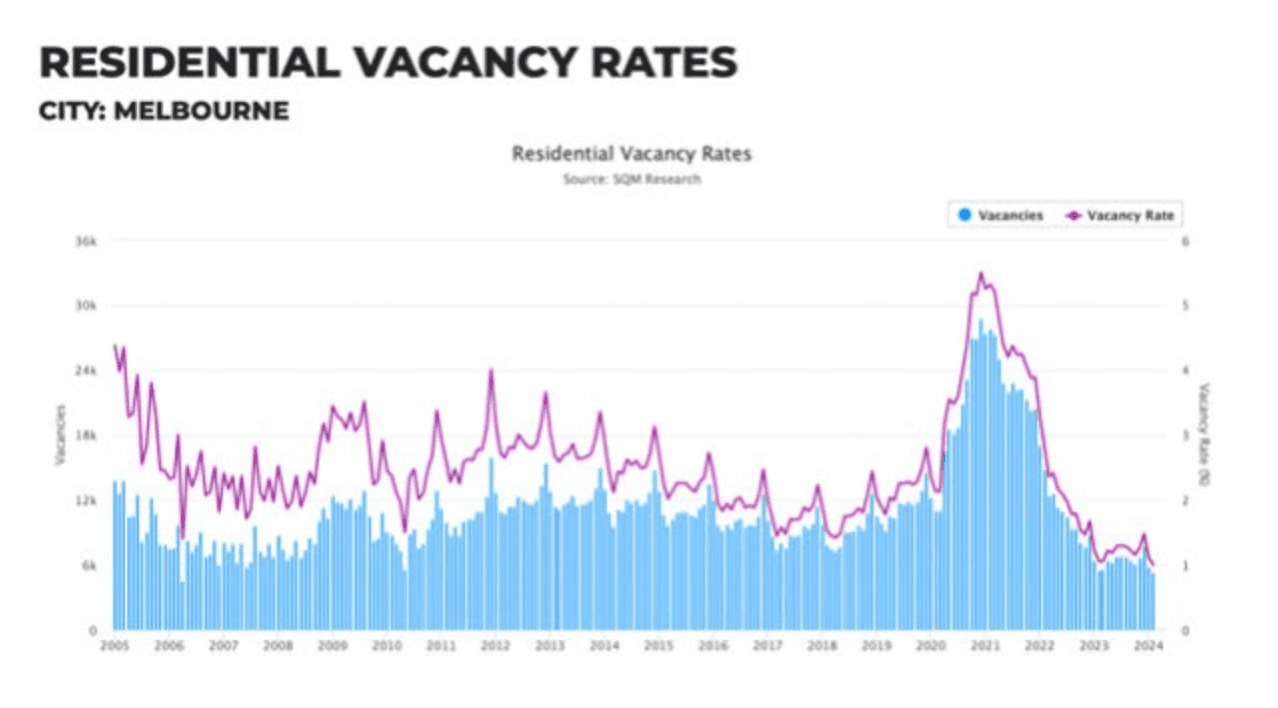

This is further indicated by Melbourne’s rental vacancy rates, which have remained persistently low across 2023 and into 2024:

So, in reality, we’re actually witnessing a simultaneous over and under supply of property, within the same market.

A chronic undersupply of rental properties, alongside an oversupply of properties for sale, due to a discrepancy between the levels of underlying vs purchasing demand for homes.

It’s an incredibly interesting set of circumstances!

For prospective investors, this also represents a particularly compelling opportunity, given that such factors are indicative of a market that will be hypersensitive to interest rate changes.

With the rate cuts expected later this year, we could well see property prices in Melbourne react with more exuberance than in other capital cities.

Make confident property investment decisions. Book a free consultation with a buyer’s agent today.