- The first step is making the call.

- 1300 022 482

- hello@searchpartyproperty.com.au

30th November 2023 – Property Market Update

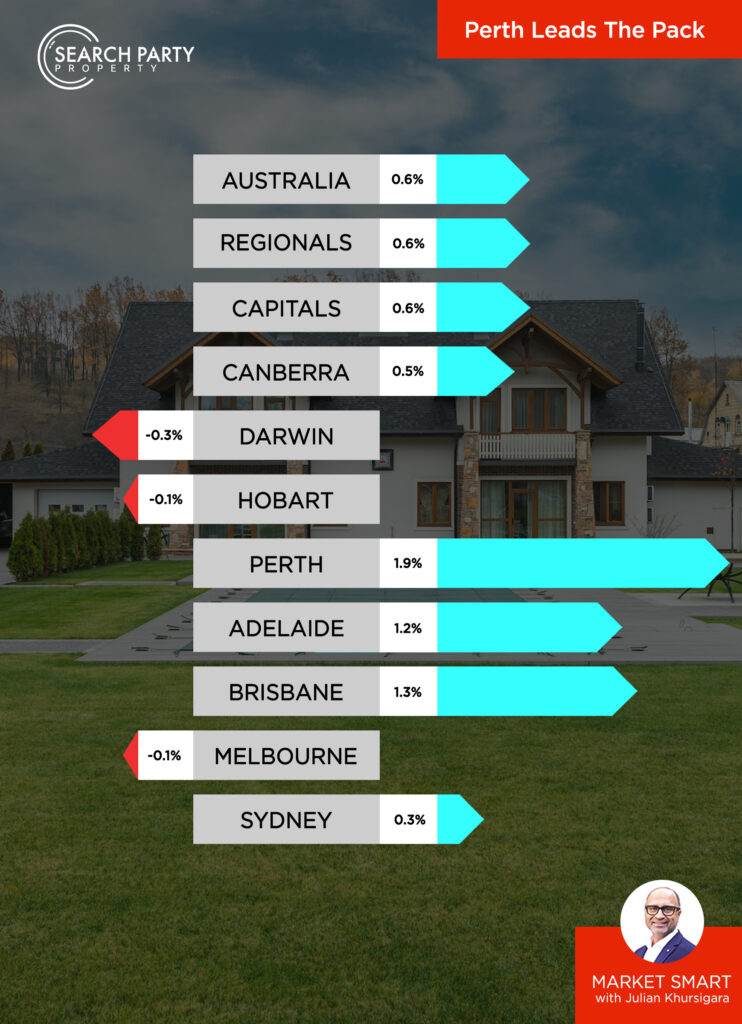

Perth Leads the Pack

This month’s Market Smart highlights a growing contrast between overall slowing growth and the exceptional performance of a select few regions – especially Perth, which remains the fastest growing city in the country. CoreLogic’s national Home Value Index rose by a modest 0.6% in November, the smallest monthly gain since February, indicating a shift in the market’s momentum. Read on as we examine the dynamic factors defining this shift and explore what it all means for investors.

Where we are now?

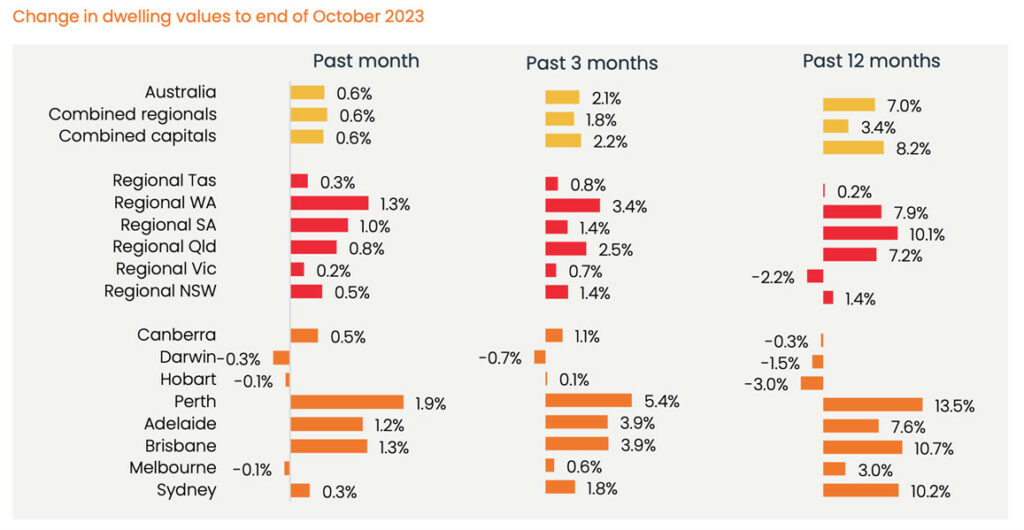

November was somewhat of a mixed bag for the Australian housing market. While a new record market value was hit (with the median national value climbing above the previous record of $768,777), November also saw the smallest monthly gain since the beginning of the growth cycle in February. However, this subtlety in growth belies the resilience of the market, which has now produced an 8.3% rebound over the past 10 months, following a 7.5% drop from April 2022 to January 2023. This recovery illustrates a clear the ‘V’ shaped recovery much hoped for by investors. Particularly noteworthy is Perth, which has surged ahead with a 1.9% rise in housing values – the most significant monthly gain since March 2021. In contrast, cities like Melbourne and Sydney show signs of cooling, with Melbourne experiencing a slight decline and Sydney’s growth decelerating.

“Multi-speed” conditions became increasingly prominent across November, with the rate of growth actually accelerating for Perth, along with continued growth in Brisbane and Adelaide. Meanwhile, Darwin, Melbourne and Hobart have all contracted, with Sydney relatively stagnant but not far behind.

Another noteworthy development has been the trajectory of regional markets relative to the capitals. Having lagged the major cities since the national market began to recover from its January low, regional markets rose 0.6% in November, the same result as aggregate capital growth. The sluggish pace of regional markets throughout 2023 means that they haven’t yet completed a similar V-shaped recovery – being currently 1.8% below record 2022 highs.

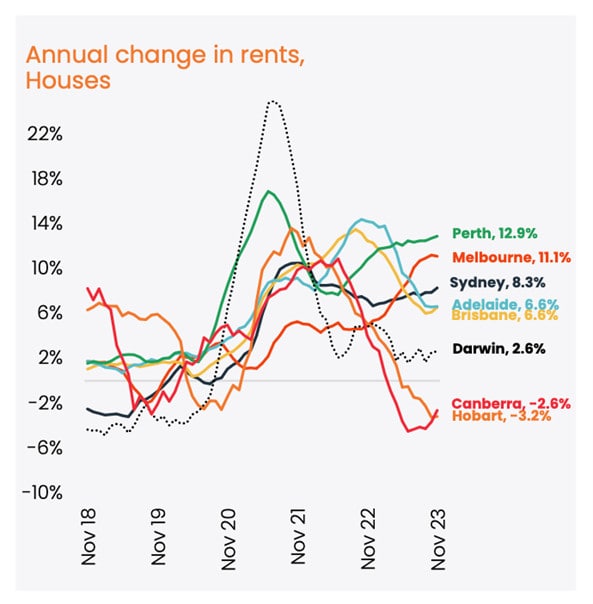

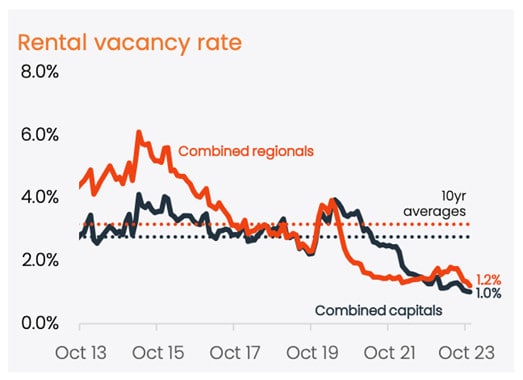

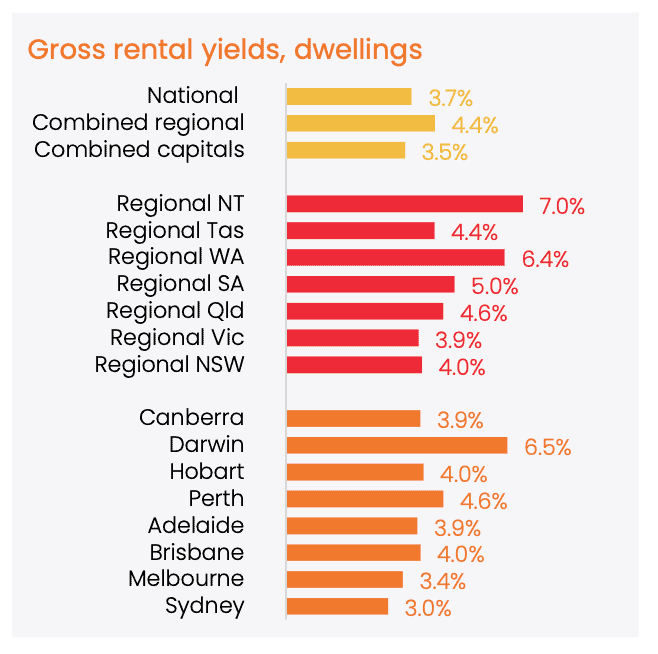

The rental market has remained remarkably tight through November, with capital city vacancy rates averaging at a low of 1.0%. This tightness is exemplified by cities like Adelaide, Perth, and Melbourne, which are recording some of the lowest rental vacancy rates. Adelaide stands out with a strikingly low rate of 0.3%, followed by Perth at 0.6% and Melbourne at 0.8%. Fascinatingly, November also marks the first time in six months that rents have grown faster than home values.

How did we get here?

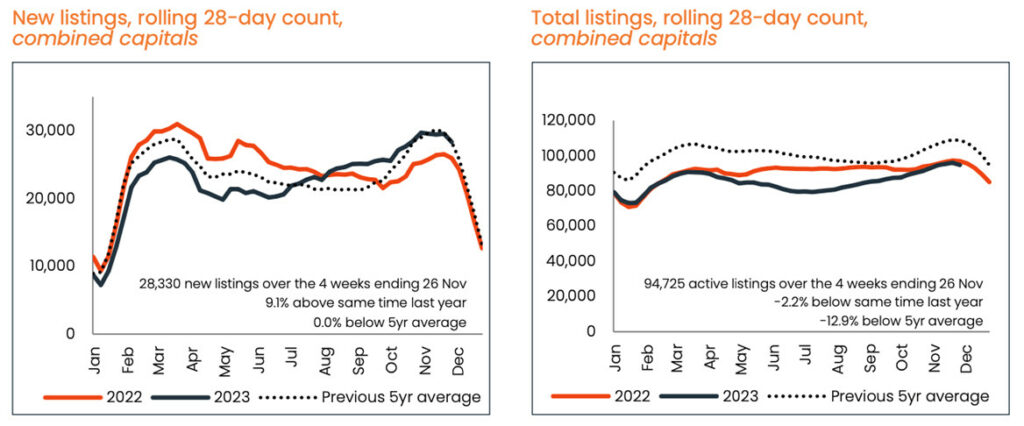

Winter saw a significant rise in vendor activity, which is seasonally unusual. This surge in new listings, following a prolonged period of below-average levels, coincided with the slowing growth in home values. Higher stock levels have been observed since July, indicating that purchasing demand isn’t quite keeping pace with the increase in vendor activity. This shift has resulted in more buyer-friendly market conditions in cities like Hobart, Canberra, Melbourne, and Sydney, where buyers now have more choices, less urgency, and greater opportunities to negotiate.

November saw Melbourne, Hobart, and Darwin experienced slight declines in their housing values, contrasting sharply with the robust growth in Perth. This divergence illustrates the multi-speed conditions increasingly evident across the capitals. In Sydney, there has been a notable deceleration, with the smallest monthly gain through the recovery cycle to date. Interestingly, these patterns track almost perfectly variations among listing levels, which in Perth remain 40% below five-year averages, and in Brisbane and Adelaide are 30% below five-year averages. It’s unsurprising then that Perth leads Brisbane and Adelaide as the three fastest growing markets in the country.

Other factors have also played a big role. The Melbourne Cup Day rate hike alongside worsening affordability, rising advertised stock levels, and persistently low consumer sentiment have collectively acted as a drag on value growth in some markets. The stifling effect of these conditions upon demand is having an especially pronounced effect upon growth within those markets with supply levels already at or around historic levels.

Continued scarcity in rental properties has consequently driven up rents, a trend that has been persistent since August 2020. For over 40 months, rents have been on an upward trajectory, with the trend intensifying in the last two months. Notably, Perth has led the nation in rental cost growth, with house rents increasing by 3.1% and unit rents by 3.4% over the three months ending in November. This sustained increase in rents, outpacing the growth in home values for the first time in six months, has provided some support to the gross rental yields nationally, although the yields remain compressed due to high debt costs and maintenance expenses.

Where are we going?

Looking ahead through December and out to 2024, forecasts are becoming more complex, with ‘multi-speed’ market conditions likely to persist. Perth and Brisbane look set to offer some degree of certainty though, with sustained growth seeming a likely outcome. Regardless, here a few trends to keep an eye on concerning the national markets.

Interest Rates

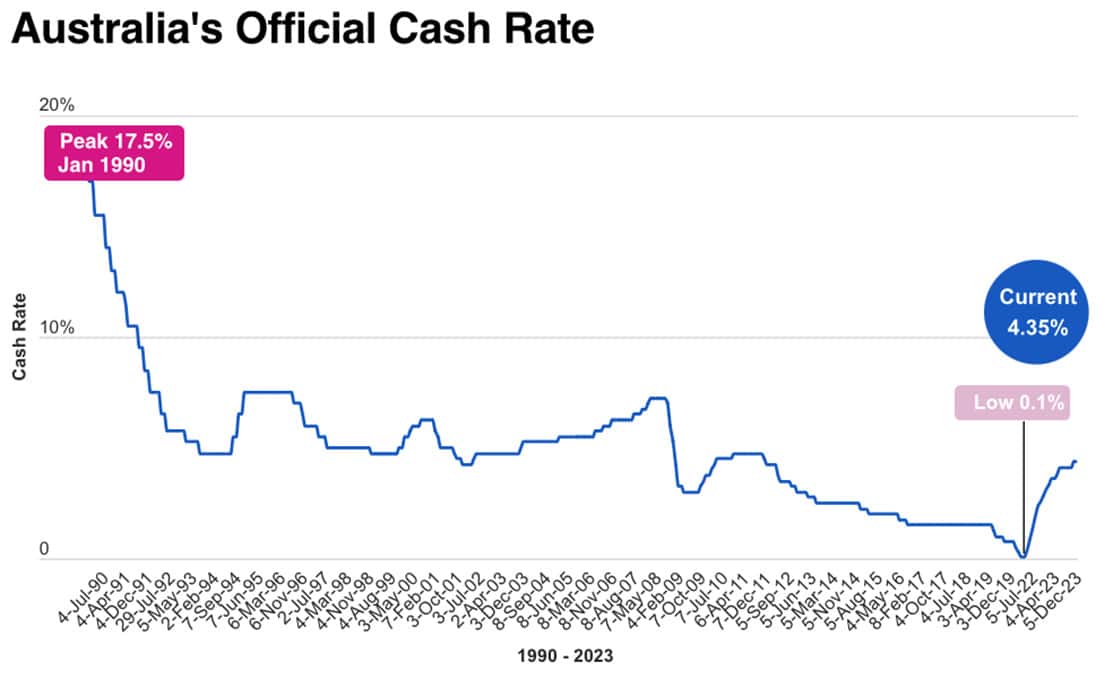

On the 5th of December we learned of the RBA’s final decision for 2023 – that interest rates would be held at 4.35%. Following last month’s raise, this means interest rates will remain at their highest level since 2011, until at least February when the RBA next meets.

RBA Governor Michele Bullock has insisted that the decision was based upon positive inflation signs, though cost of living concerns may have also played a major role. Since the rate hike cycle began last year, a $600k mortgage is now costing borrowers an additional $1,349 per month and last month, research conducted by Digital Financial Analytics found that 2 million households are currently spending more than they earn.

With inflation having fallen to 4.9%, a positive sign, CBA and Westpac are both predicting that the cash rate will have now peaked before cuts arrive in late 2024. However, expectations are mixed – AMP economists have warned of the potential for an additional 25 basis point rise in February, citing a ~45% chance.

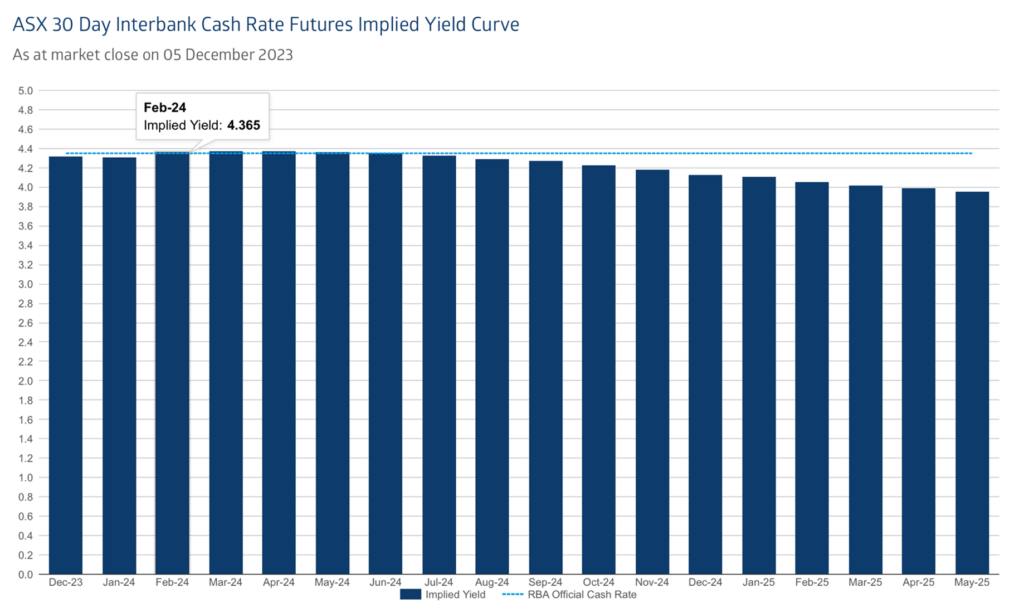

Similarly, futures markets are currently supportive of a non-zero chance for a February rate hike:

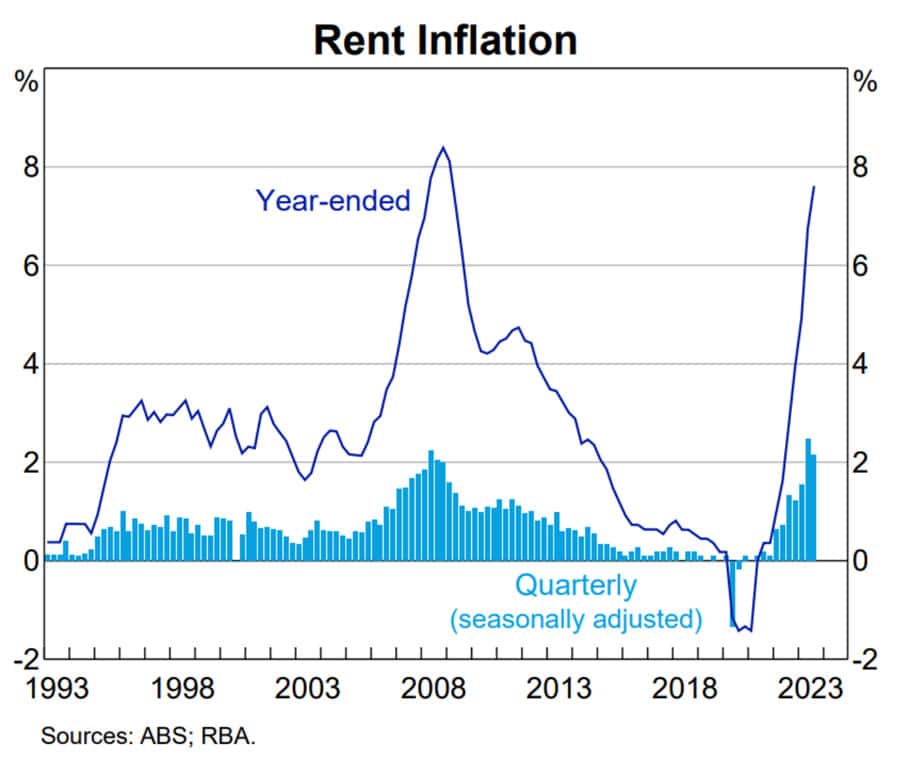

Rental Inflation

As we reported not long ago, it’s recently become cheaper to buy a home than rent in much of the country, as rental inflation has been staggering. We’re currently experiencing the fastest growth in rent since 2008, driven primarily by immigration levels:

Economic Performance

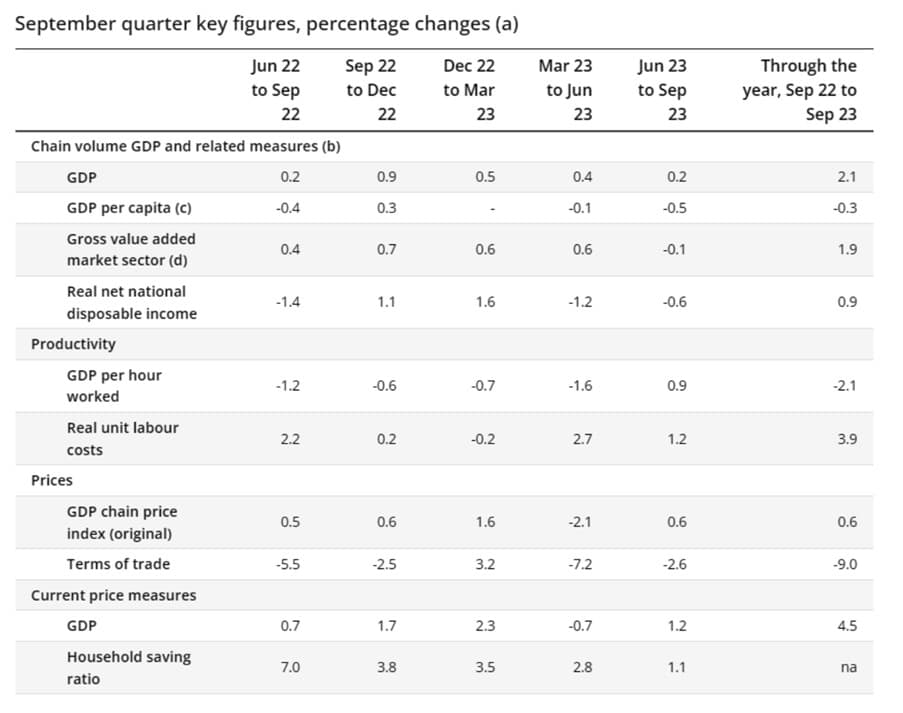

Following the release of the national accounts by the ABS, the reality of the country’s poor economic performance has become clear.

While GDP rose 2.1% across the year preceding September 2023, GDP has fallen on a per capita basis across the same period by 0.3%. For three of the last five quarters, real GDP per capita has been in a downward trajectory. If not for high migration figures, Australia would currently be in a definitive recession – which adds another layer of complexity to the RBA’s pending decision in February next year.

At Search Party Property, we specialise in developing tailored investment strategies and will work with you to come up with a suitable plan of attack. We also regularly assess your strategy ensuring that it is fit for purpose and delivering the desired results.

{kind=link}

{kind=link}

{kind=link}