- The first step is making the call.

- 1300 022 482

- hello@searchpartyproperty.com.au

31st December 2023 – Property Market Update

December Market Smart – Positive Signs for 2024

It’s our last Market Smart for 2023! As we look ahead to 2024, the real estate landscape is demonstrating plenty of encouraging signs. The past year has been a period of notable growth, with national home values producing an exciting rebound. Within this national rebound has been a diverse set of outcomes across various markets, indicating some nuanced but encouraging signs. In this report, we’re dissecting some of the factors that fuelled December’s market performance, and casting an eye towards the year ahead.

Where we are now?

A new record for national values has been set, following November’s peak, highlighting the strength of the market's recovery. Despite the smallest monthly gain since this growth cycle began in February, December’s modest 0.4% has produced an overall 8.1% boost for property across 2023. Despite December being the smallest rate of growth since February, a further slowing of November’s 0.6% growth, the continued upward trajectory has produced a significant turnaround from 2022’s -4.9% decline in values.

Perth continues to emerge as a frontrunner, with housing values rising by 1.6% — rising by less than in November – now up to a leading 15.2% growth across 2023. This is but one gauge of a broadening disparity between a handful of capital cities and the rest of the country. Perth, Adelaide and Brisbane have all averaged 1% growth each month since May, while Sydney and Melbourne continue to experience relative stagnancy and some contraction fuelled by the rate hike cycle.

Capital cities, on the whole, have outperformed regional areas, with a 9.3% rise in the capitals against a 4.4% increase in regional indices. This shift reflects the normalisation of regional migration trends and the affordability challenges emerging from the significant capital gains recorded in prior years. However, interestingly, regional markets in December did actually outperform Sydney, Hobart, Canberra and Melbourne. Clearly, Perth, Adelaide and Brisbane are doing the heavy lifting. Five of the eight capitals are still below their record highs, with cities like Sydney and Melbourne not yet recovering to their peak levels from previous years.

Source: CoreLogic, 2024

Perhaps nothing exemplifies these ‘multi-speed’ conditions better than comparison of capital city performance since COVID. Perth, Brisbane, and Adelaide are all up ~50% since the onset of COVID and are all currently at record highs. All other capital cities are lagging well below 50% growth across the same period and are well below record values.

Source: CoreLogic, 2024

Last year saw an 8.3% increase in rents nationally, a slowdown from the rates seen in the previous two years. Despite the deceleration, this growth was still notably higher than the pre-COVID decade average, indicating a strong market in the context of the long-term trend. Divergence was again a key theme, with unit rents growing faster than house rents, yet

showing signs of a slowdown, potentially due to a softening in overseas migration and the impact of renters reaching their affordability limits.

Regionally, the rental market’s growth decelerated to 4.3%, the smallest annual rise since before the pandemic, attributed to the normalization of migration trends and an inherent easing from previously high rent values. Perth stood out with continued strong growth in rents, contrasting with places like Hobart and Canberra, where rents declined. This variance highlights the uneven impact of economic forces across different markets and housing types.

As we approach 2024, the rental market is likely to experience continued growth, albeit at a potentially slower pace, as affordability challenges could lead to changes in rental demand patterns, such as an increase in group households or multi-generational living arrangements. The outlook is influenced by a complex interplay of factors, including interest rates, economic conditions, and migration trends, all of which will shape the trajectory of the rental market in the coming year.

How did we get here?

As 2023 unfolded, the Australian housing market witnessed a noticeable shift in supply dynamics, particularly in the volume of new and total listings. The end of the year saw new listings in the combined capitals slightly above the numbers from the same time last year, yet precisely aligned with the five-year average, indicating a stabilization of market entry rates.

This tightening has been instrumental in shaping market conditions across different cities. With overall listings not keeping up with new entries, the market has seen varied effects on housing values. In cities like Perth, a substantial deficit in listings compared to the historical average has likely contributed to the strong growth in housing values. This contrasted with the trends in Melbourne and Sydney, where housing values have shown signs of stability or marginal decline, influenced by a closer alignment to average listing volumes.

These supply factors, coupled with macroeconomic influences such as the rate hikes and associated affordability challenges, have forged the current market landscape. The culmination of these elements provides the backdrop for the distinct ‘multi-speed’ conditions observed across the capital cities, with disparate growth trajectories reflecting the unique interplay of local demand and supply nuances. A major response to low rental supply has also not yet occurred, with multi-generational households becoming more commonplace.

Nationally, gross rental yields for dwellings settled at 3.7%, reflecting the relationship between rental incomes and property values across the country. In the combined capital cities, these yields were slightly lower at 3.5%, while regional areas offered a slightly more attractive yield at 4.4%. These figures suggest that despite the rise in property values, rental incomes have proportionately increased, offering a stable yield environment for investors. This balance is crucial, especially in an economy witnessing varied growth in home values and rents, and where investors are keenly observing market trends to maximize their returns. The sustainability of these yields, however, will likely hinge on the trajectory of both property values and rental rates in the forthcoming year.

Where are we going?

As we predicted earlier last year, 2024 is increasingly looking like a year of two halves for property, with an excellent window of opportunity now open for investors.

A year of two halves

The first half of the year looks set to unfold under the shadow of 2023’s cooling market trends, with early indicators pointing towards a more subdued outcome for housing values. High interest rates and a softening economic landscape, exacerbated by lower consumer spending and a more flexible labour market, are expected to dampen market activity. This was prefigured in the latter part of 2023, with Melbourne’s housing values trending downwards and Sydney’s growth slowing considerably. Even Brisbane and Perth – cities previously marked by robust performance, saw a deceleration in growth as the year closed.

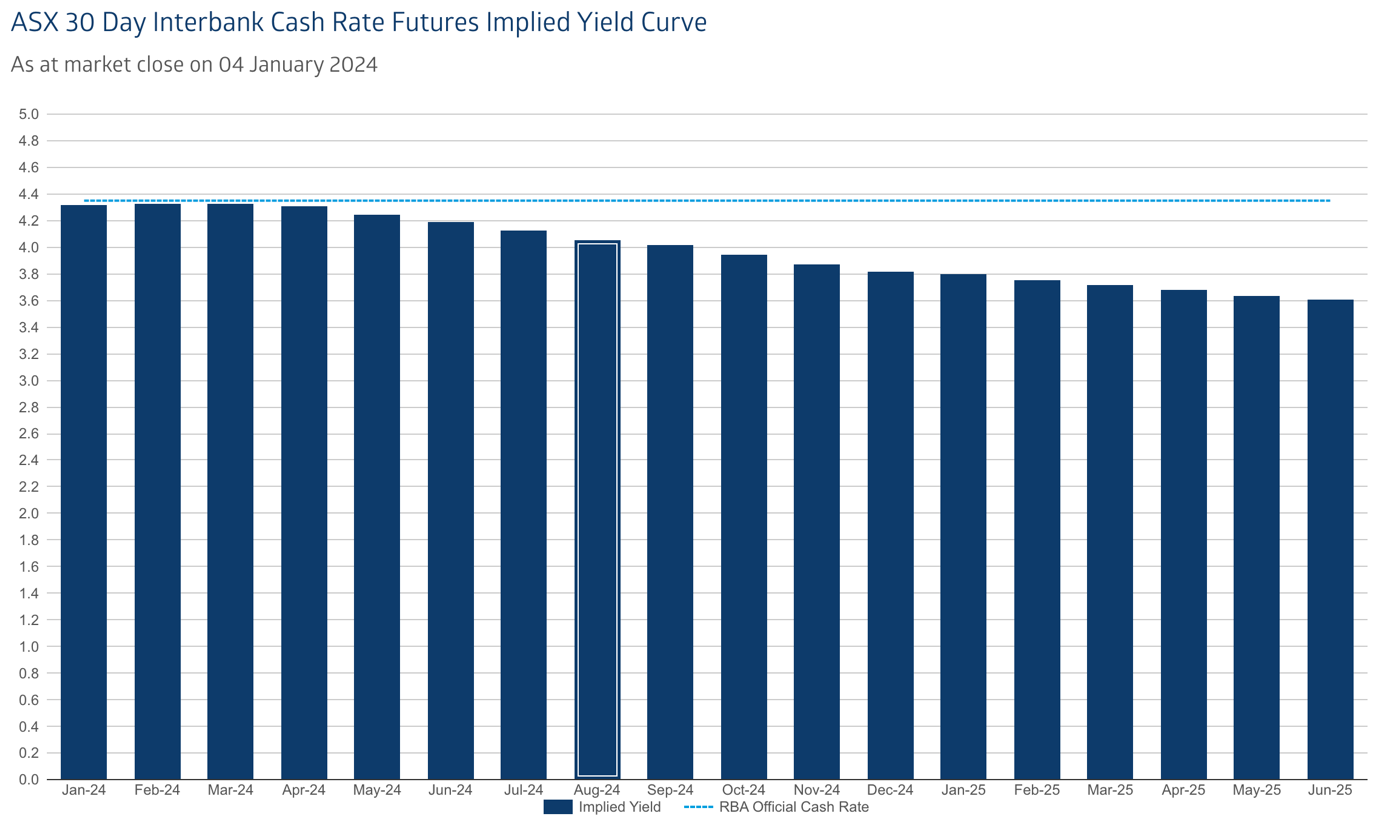

The course of interest rates throughout 2024 will play a pivotal role in shaping the property market’s direction. While the threat of further rate hikes looms, the prevailing economic indicators suggest they may be less likely, with inflation showing signs of easing and economic conditions weakening. Should the RBA choose to lower the cash rate, as financial markets are anticipating with a rate cut expected by mid-year, we could witness a revitalization of consumer sentiment and an uptick in housing activity and values in the latter half of 2024. Particularly in markets like Perth, Adelaide, and Brisbane, already defying rate hike factors, we could see a period of particularly notable growth throughout the second half of 2024.

Source: ASX, 2024

Housing affordability will continue to be a key concern, with the latest reports indicating a deterioration in affordability metrics across the board. The government’s pledge to address this through the delivery of 1.2 million new homes over the next five years is unrealistic, and will test the construction sector’s capacity, particularly against a backdrop of tight profit margins and resource scarcity. The $10 billion Housing Australia Future Fund signals positive steps towards alleviating the affordable housing shortage. However, the lag between the high rates of overseas migration seen last year and the consequent rise in purchasing demand may take some time to manifest in the market, potentially buoying housing prices to a certain degree over the year. As these various factors converge, they point to a complex and potentially bifurcated market landscape for 2024.

At Search Party Property, we specialise in developing tailored investment strategies and will work with you to come up with a suitable plan of attack. We also regularly assess your strategy ensuring that it is fit for purpose and delivering the desired results.

{kind=link}

{kind=link}

{kind=link}