- The first step is making the call.

- 1300 022 482

- hello@searchpartyproperty.com.au

31st July 2023 – Property Market Update

Market Resilient – Brisbane and Perth continue to grow

Join us as a we take a quick look at the Australian property market throughout July 2023. We’ll point out the highs, the lows, and everything in between across our capital cities. We’ll also delve into the forces that have been driving these changes and share our thoughts on where we are heading in the months ahead.

Where we are now?

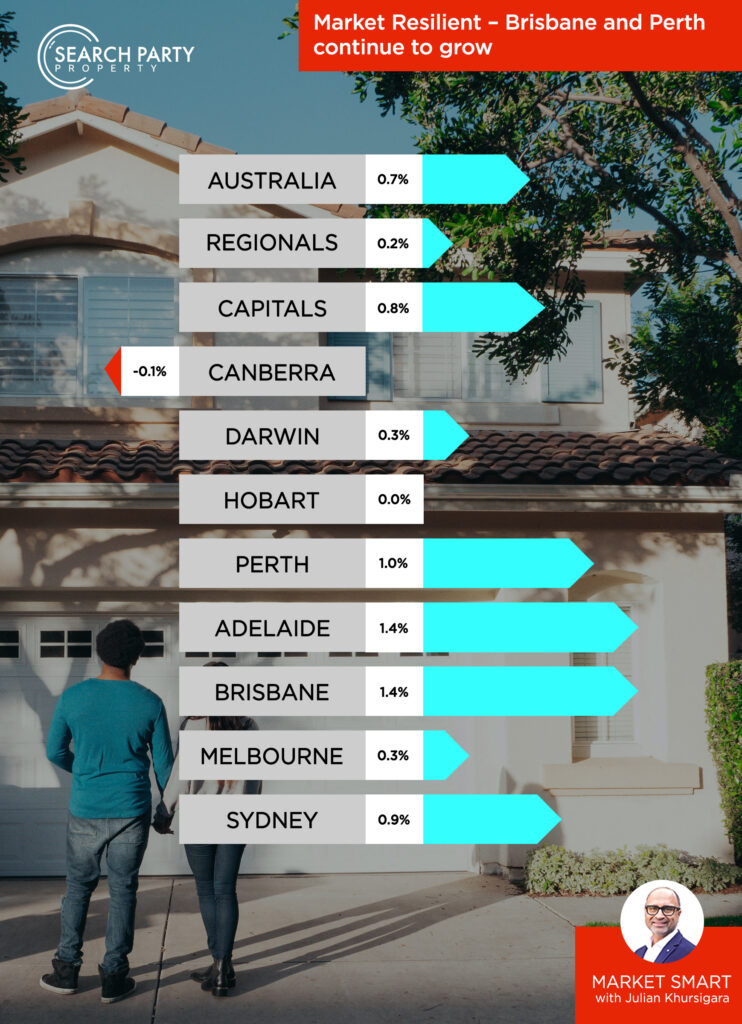

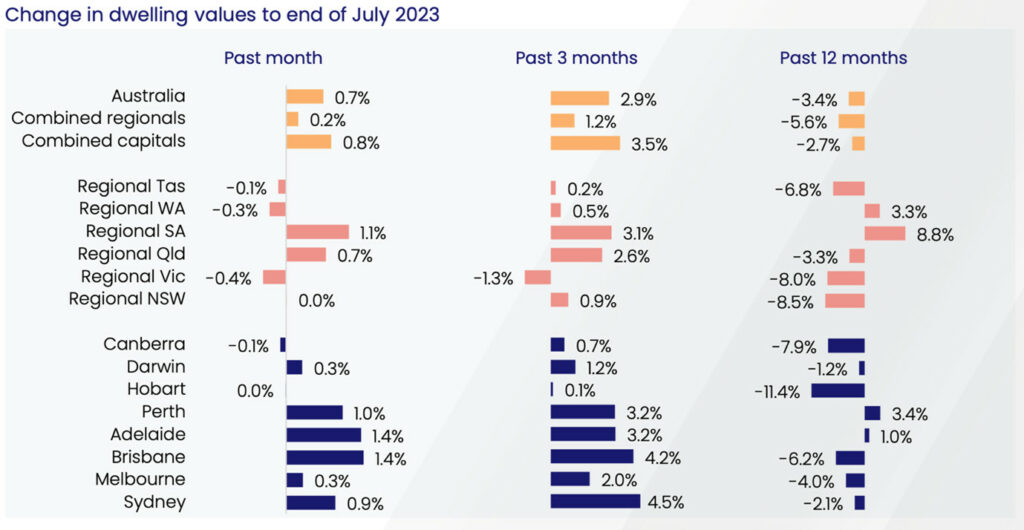

- Sydney: The rate of price growth in Sydney has slowed significantly, falling by almost half from 1.7% growth in June, to just 0.9% growth in July.

- Melbourne: Similar decline in rate of growth, falling from 0.7% growth in June to a near-stagnant 0.3% in July.

- Brisbane: Price growth in Brisbane has accelerated with 1.4% growth, up marginally from 1.3% in June.

- Adelaide: More significant rises in Adelaide with the rate of growth hitting 1.4%, up from a more modest 0.9% movement in June.

- Perth: Overall a fairly stagnant month for price growth in Perth, with just 1% growth only a 0.1% bump from June.

- Hobart: No aggregate change whatsoever in Hobart, climbing out of a 0.3% decline in prices across June.

- Canberra: The only city to decline overall this month, Canberra prices have fallen 0.1%, after a 0.4% rise in June.

- Darwin: Down slightly from 0.5% price growth in June to only 0.3% in July.

How did we get here?

- The Supply-Demand Balance:

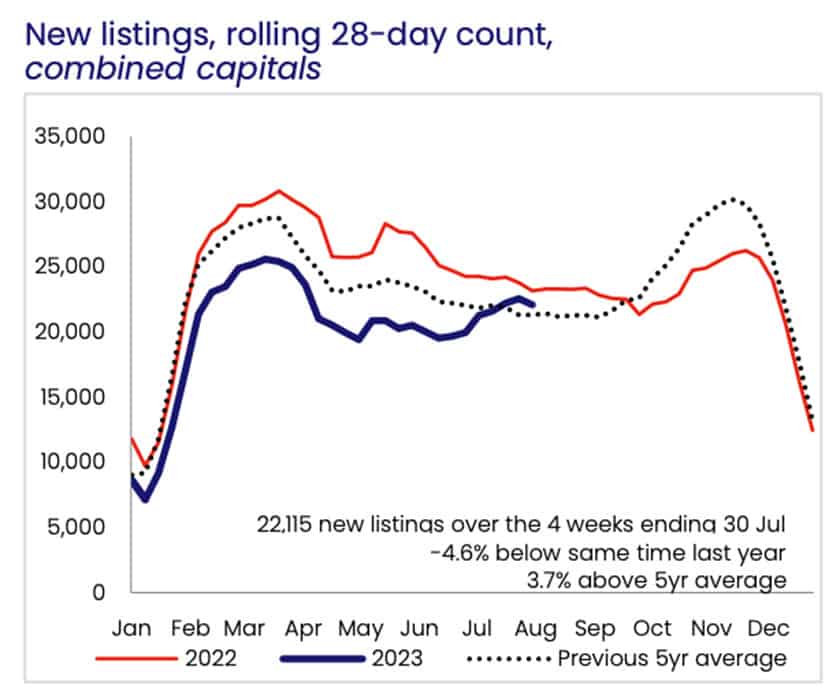

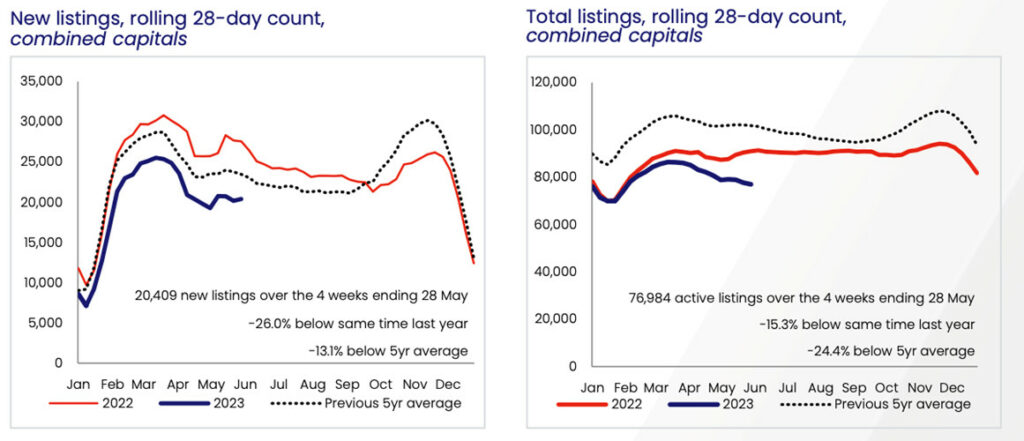

In the four weeks leading up to July 30, there was a 3.9% increase in new listings in the capital city housing market. This is unusual for the winter season, which typically sees a decrease in new listings. Despite this increase, the total number of listings remains 18.3% lower than the same time last year and 23.3% lower than the five-year average. This suggests that the demand for housing is still outpacing the supply, contributing to the continued rise in housing values.

- Favourable Selling Conditions:

The rise in new listings hasn’t led to an oversupply, as the total number of listings remains significantly below average. This suggests that the market is still very much in favour of sellers. Some homeowners may be taking advantage of these conditions by choosing to sell now rather than waiting for the typically busier spring season.

- Potential Rise in Advertised Housing Stock

The number of new listings has been below average since September of last year. However, with total stock levels still low and selling conditions favourable, more homeowners may choose to sell now rather than wait until the spring season. This could be due to a desire to take advantage of the current market conditions or a response to the rapid rate hiking cycle’s impact on household finances.

- Revival of Buyer Activity

Despite the backdrop of the highest interest rates since 2012 and consumer sentiment levels reminiscent of the Global Financial Crisis, there’s a notable resurgence in buyer activity in the housing market. Data up to May reveals a significant uptick in home loan commitments, reaching a peak not seen since August of the previous year. This surge aligns with an upward trend in the value of lending that began in March, mirroring the concurrent rise in home values.

This rejuvenated demand isn’t just reflected in lending data but is also evident in sales activity. Estimates suggest that sales over the recent three-month period have modestly surpassed the average of the past five years. This indicates a robust demand that persists despite the challenging economic climate, underscoring the resilience and appeal of the housing market.

Is the growth here to stay?

As always, the question remains – for how long will these current market conditions persist?

Here are some factors that could influence the market’s trajectory:

- Housing Undersupply

The forecasted undersupply of around 175,000 dwellings by 2027 is a significant concern for the Australian housing market. This shortage is not just a number; it represents a multitude of potential issues, including increased competition for available homes, higher prices, and a potential increase in homelessness. The undersupply is likely to be driven by a combination of factors, including population growth, migration patterns, and the pace of new housing construction. If these predictions hold true, we could see a sustained period of price growth, as demand continues to outstrip supply. However, this could also lead to increased policy focus on boosting housing construction and could present opportunities for investors and developers in the housing sector.

- Mortgage Arrears

The prediction of an increase in mortgage arrears in the second half of the year is a worrying sign. As variable rates tend to follow the cash rate with a lag, more borrowers are expected to feel the pinch of rate hikes. Over the next few months, many homeowners will start to feel the impact of recent rate hikes and more than 800,000 home loans are expected to transition from low fixed rates to variable rates of around 6% or higher.

On an individual level, this is likely to lead to financial stress and potential home loss for some of those affected. While it could lead to an increase in mortgage arrears, the extent of this will depend on the state of the labour market interest rates. It could of course lead to an increase in forced sales, which could put downward pressure on house prices, and impact the balance sheets of banks and other lenders.

- The rate pause – A change in RBA approach?

On the 1st of August, the RBA made its first ruling on interest rates since last month’s announced change in leadership. Interest rates were held at 4.1%, marking the first instance of a consecutive rate pause since May last year. The move took markets and many leading economists by surprise, with the Australian dollar plunging 1.5% against the US dollar – the lowest fall since March.

Prior to the announcement, predictions were split. Bond markets were estimating only a 24% likelihood of an interest rate hike, indicating an imminent pause. However, in a survey conducted by Refinitiv, a majority of economists polled anticipated that the central bank would implement a 13th rate increase in the current cycle.

Despite the slight relief for homeowners however, the move has drawn significant criticism and left many speculating on a change in the RBA’s approach to rate setting.

Warren Hogan, chief economic adviser at Judo Bank, said the decision indicates that the Reserve Bank is “not determined to bring inflation down” and “has completely given up on being pre-emptive.” Mr Hogan cited the RBA’s the latest announcement, with the RBA curiously indicating that it has pushed back its original timeline for returning to 2-3% inflation, by an additional 6 months to late 2025.

“Basically, what they’re saying is we’re not raising rates, we’re going to live with inflation for longer,” Mr Hogan said. “That has a range of implications, not least that it’s going to bring the misery to the broader community for longer.”

Meanwhile, Peter Tulip, chief economist at the Centre for Independent studies, also expressed concerns that both the labour and housing markets remain overheated.

“While I don’t think [August’s monetary policy] decision was a surprising decision, I also think it was a disappointing decision,” Mr Tulip said. “Previously when we’ve had an unemployment rate of 3.5%, like in 2008 or the 1970s, that’s been accompanied by rapidly accelerating prices and wages, and essentially it’s got out of control” (savings.com.au, 2023).

It will certainly be interesting to continue to observe the trajectory of inflation and interest rates over the coming months as the RBA transitions to new leadership in September.

At Search Party Property, we specialise in developing tailored investment strategies and will work with you to come up with a suitable plan of attack. We also regularly assess your strategy ensuring that it is fit for purpose and delivering the desired results.

{kind=link}

{kind=link}

{kind=link}