- The first step is making the call.

- 1300 022 482

- hello@searchpartyproperty.com.au

Is a Property Crash Inevitable?

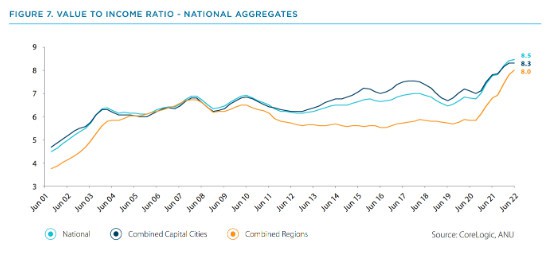

As of most recent mid-2022 figures, it was reported that Australia has “the third-highest house price-to-income ratio in the world” up at 8.5. Back in June 2001 this figure was just 4.5:

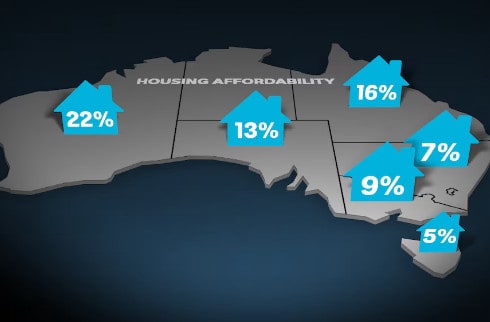

In Tasmania, an average wage is currently enough to afford just 5% of homes, the lowest percentage of any state, though it isn’t a whole lot better elsewhere.

According to a recent PropTrack report, even a six-figure income is enough to afford just 13% of homes, while a household income of $64,000 a year is enough for only 3%.

Current forecasts indicate that these figures will continue to deteriorate.

In as little as two years from now, first time buyers could be priced out of all but three suburbs in Melbourne, with consultancy firm KPMG predicting a median price north of $1 million by mid-2025, alongside similar expected trends elsewhere.

According to CoreLogic’s head of research, Eliza Owen:

“Property prices are expected to keep rising as interest rates stay on hold, and they could increase faster once interest rates start coming down next year, which means first home buyers would need to save a bigger deposit, which would take a lot longer”.

While this might be good news for those already invested, the picture looks increasingly bleak for those trying to enter the market.

But what is the endgame of a continued fall in affordability? If prices continue at this rate, are we due for an inevitable correction? Or to put it another way – if nobody can afford a home, who’s going to buy them?

A spectacular housing crash must be on the horizon, eventually. Right?

A housing bubble?

Despite the media’s click-driven narratives, the idea of an impending crash is not new. Claims that the Australian housing market is in a bubble have persisted since at least the post-GFC early 2010s, parroted by commentators and politicians alike. However, much of this can probably be attributed to the lack of an obvious definition for what actually constitutes a housing bubble and, if there were one, what constitutes its bursting.

An economic bubble is often defined as a situation where an asset has become grossly overvalued, where its price has detached from being an accurate measure of intrinsic value. Similar to other concepts in economics like recessions, bubbles don’t have a universally agreed upon empirical definition.

There just isn’t a definitive milestone that tell us, ‘Yes, you are now in a housing bubble’, because it’s difficult to know when something can be called overvalued. After all, the price of something is its price. We don’t have a secret, real price to compare against.

All anyone can do is make arguments as to why a price seems probably higher than it should be. For housing, measures of affordability make a pretty decent gauge for this. If the average person can’t afford to buy the average house, then it’s probably reasonable to conclude that housing is overvalued. In view of some of the affordability statistics we’ve just discussed, there must then be some credibility to the idea that Australian housing is in a bubble.

In fact (stopping just short of using the ‘B’ word) the IMF has identified the Australian housing market as high risk, behind only Canada as the riskiest in the world. However, accurate though it may be as a descriptor of current factors, the ‘high risk’ classification still doesn’t give us a firm answer to our crash question. It’s certainly possible for price rises to persist amidst greater underlying risk, defying expectations.

The long-term trajectory of a market plagued by affordability concerns remains a very difficult question to answer, as evidenced by the earlier half of 2023. Back in May the big four banks were all somewhat embarrassingly forced to revise their predictions of a continued fall in house prices, and their latest predictions are all contradictory: CBA predicting a slight rise, NAB a slight fall, and ANZ and Westpac predicting stagnant prices.

Two Scenarios

Now, having just pointed out the notorious difficulty of market predictions, time for some of our own!

In an attempt to try and answer whether or not a crash is inevitable, here are two loose scenarios to consider.

1. Status quo growth:

For at least the next few years a crash seems highly unlikely, irrespective of the affordability concerns. Rather, it’s more probable that prices will continue to rise.

The reason for this is a continued imbalance in market fundamentals which looks unlikely to resolve any time soon. As we’ve commented on in market reports, housing supply levels are simply insufficient for demand and astonishing immigration figures are only adding to this disparity.

Though we can’t claim to predict exactly how long this situation may persist for, the government’s supply-based affordability initiatives are shaping up to be an exercise in futility, and it’s important to remember that the current run of price rises have continued despite the highest cash rate in a decade. One wonders what new heights prices could leap to when interest rates do finally soften, potentially as early as mid-2024, according to some.

2. If a correction does (eventually) happen:

Based on what we’ve discussed, it’s certainly a big ‘if’ anytime soon.

Though as the IMF has pointed out, high underlying risk driven by affordability, means it will remain a remote possibility into the future. However, if a correction does occur, it’s unlikely to be a dramatic crash – rather, a gradual easing of affordability.

This thinking is grounded in the recognition that historically, dramatic housing crashes have been associated with a different set of factors – notably, an excess of housing supply.

For instance, take the United Kingdom and Japan in the 1990s, and more recently, Spain and Ireland in the 2010s. In these cases, an overabundance of available housing stock significantly exacerbated the effects of their respective housing market crashes. High levels of supply combined with sharp reduction in demand led to rapid price declines and prolonged economic repercussions.

For Australia currently, the market dynamics present a marked contrast to these examples. We’re currently grappling with an undersupply of housing, exacerbated by robust population growth, particularly in major urban centres. Moreover, Australia’s housing market has shown recent resilience, emerging unscathed from a cash rate stress test. It all points to a unique degree of robustness and adaptability, regardless of a worsening of the same affordability concerns that have persisted for over two decades. Given these factors, it seems likely that the Australian housing market may be more inclined towards a gradual slowdown or a level of price stagnation rather than a precipitous crash.

This being true, the old moniker of ‘time in the market beats timing in market’ is likely to remain the propitious strategy, in favour of those delaying a purchase in the hopes of an imminent flash sale on real estate. Overall though, in navigating the complex terrain of the property market, one thing remains clear: the need for expert advice and guidance has never been more critical.

Want to discuss this further?

For expert guidance in property strategy, and what it could mean for you as a property investor, book in for a free consultation to make informed decisions, tailored to your investment goals. Don’t let affordability challenges hinder your success. Act now with Search Party Property!

{kind=link}

{kind=link}

{kind=link}